For generations, real estate has been a cornerstone of wealth creation. It’s a tangible asset you can see and touch, one that works for you in two powerful ways at once: generating a steady stream of income month after month while its underlying value grows over the long haul.

It's a beautiful system, really. You acquire an asset that, when structured correctly, can essentially pay for itself and then some, all while building your net worth behind the scenes.

In This Guide

Your Blueprint for Building Real Estate Wealth

So, where do you begin? Right here. This isn't just a guide about buying property; it’s about understanding the engine that drives real estate wealth. The most successful investors I know didn't just get lucky—they learned how to harness four distinct forces that work together to create incredible financial momentum.

To put it in perspective, think about the sheer scale we're dealing with. The global real estate market is the largest store of wealth on the planet. This guide is your map to claiming your own small piece of that enormous pie.

We'll start by breaking down the core principles. Before we get into specific strategies or complex financing, you have to nail the fundamentals. These are the pillars that hold up every successful real estate portfolio.

The Four Pillars of Wealth Creation

Every savvy real estate investment is built on a foundation of four key wealth-building mechanics. Grasping how these interlock is the first and most crucial step toward making smart, profitable decisions.

Let's lay them out.

The Four Pillars of Real Estate Wealth

| Wealth Pillar | How It Works | Primary Benefit |

|---|---|---|

| Cash Flow | The money left over from rental income each month after paying the mortgage and all operating expenses. | Puts predictable, consistent income in your pocket, creating financial stability. |

| Appreciation | The property's market value increasing over time, driven by inflation, demand, and local improvements. | Builds your long-term net worth and creates a substantial chunk of equity. |

| Loan Paydown | Your tenants' rent payments cover the mortgage, systematically paying down your loan balance for you. | Builds your equity automatically, almost like a forced savings account paid by someone else. |

| Tax Advantages | Deducting expenses like mortgage interest, property taxes, and even the "paper loss" of depreciation. | Legally reduces your taxable income, letting you keep more of what you earn. |

When you get these four pillars working in concert, you unlock the true power of real estate investing. It's a formula for sustainable, long-term growth.

As we move forward, we'll explore the practical strategies you need to put these principles into action. Our comprehensive https://topwealthguide.com/real-estate-investment-guide/ dives even deeper, offering more context for those just getting their feet wet. You're about to see firsthand why real estate has stood the test of time as one of the most reliable wealth-building vehicles out there.

Finding Your Real Estate Investment Path

There’s no single, secret formula for building wealth through real estate. Anyone who tells you otherwise is selling something. The truth is, your path will look different from everyone else’s, shaped by your own financial situation, how much risk you're comfortable with, and frankly, how much time you have.

Forget the generic advice. Let's dig into the nuts and bolts of the most common strategies. We'll look at everything from hands-on rental properties and quick flips to more hands-off approaches, giving you an honest assessment of what each one really takes.

This little diagram can help you figure out where you stand right now. Are you ready to jump in, or is it time to learn a bit more?

Think of it as a simple starting point: it helps you decide whether to dive into the action or build up your knowledge base first.

Active vs Passive Investing Strategies

Your first big decision point is choosing between being an active or passive investor. It’s a fundamental split in the road. Active investing puts you in the driver’s seat—you’re the one finding tenants, screening applications, and dealing with that dreaded 2 a.m. call about a leaky toilet.

Passive investing, on the other hand, lets you put your money to work in real estate without having to manage the property yourself. You get the financial benefits without the operational headaches.

"The secret to building wealth is diversifying your assets to diversify your risk. What makes real estate so incredibly appealing for investors seeking diversification is its many options."

Neither path is automatically better; they just serve different people with different goals and lifestyles. Of course, if you’re leaning toward the active route, the very first skill you need to master is how to find investment properties. It’s the bedrock of everything that follows.

Comparing Real Estate Investment Strategies

To really get a feel for what fits you best, let's lay out the most popular strategies side-by-side. This table breaks down the key differences between popular investment methods, helping you match a strategy to your personal goals.

| Strategy | Typical Capital Needed | Time Commitment | Risk Level | Best For |

|---|---|---|---|---|

| Residential Rentals | Medium (3.5% – 25% down payment) | Medium (tenant management, maintenance) | Low to Medium | Investors seeking steady cash flow and long-term appreciation. |

| House Flipping | High (purchase + renovation costs) | High (project management, market timing) | High | Experienced investors with construction knowledge and market savvy. |

| REITs | Low (can start with <$500) | Low (similar to buying stocks) | Low | Beginners or those wanting hands-off portfolio diversification. |

| Syndications | Medium to High (typically $25k+) | Low (sponsor handles all management) | Medium | Accredited investors looking to access large commercial deals passively. |

As you can see, there are plenty of ways to get in the game. A young professional might start out by "house hacking"—living in one unit of a duplex while renting out the other. A busy doctor, on the other hand, might prefer the completely passive nature of a REIT or a syndication deal.

The global demand for real estate isn't slowing down, which speaks to its power as an asset class. Global investment volumes continue to show the market's resilience and appeal. You can dig into more of these global real estate trends in JLL's research. The strategy you choose is your ticket to tapping into this massive and resilient market.

Mastering Cash Flow and Appreciation

When it comes to building wealth in real estate, everything boils down to two core engines: cash flow and appreciation. You need to understand both to truly succeed.

Think of it this way: cash flow is your property's monthly paycheck. It’s the money that keeps the lights on and puts cash in your pocket. Appreciation, on the other hand, is the slow, steady growth of your asset’s value over time—it’s how your net worth gets built, often while you sleep.

The real art is learning how to balance these two forces. It’s what separates the pros from the people who just own a rental property. Let's dig into how each one works with a real-world example.

The Lifeblood of Your Investment: Cash Flow

Cash flow is the simplest, and I'd argue the most critical, metric in real estate. It’s what’s left in your bank account after you've collected all the rent and paid every single bill associated with the property. If it's positive, your investment is paying for itself and then some.

Calculating it properly means being brutally honest with yourself about the costs. It's so much more than just the mortgage.

Key Takeaway: True cash flow calculation must include reserves for vacancies, future repairs, and property management fees, not just the mortgage payment. Overlooking these "hidden" costs is the number one mistake new investors make.

Let's walk through a realistic scenario to see how this plays out.

Real-World Example: A Suburban Duplex

Imagine an investor, Sarah, buys a duplex for $400,000. She puts down 20% ($80,000) and gets a 30-year mortgage for the remaining $320,000 at a 6.5% interest rate.

Here's a quick look at the basic monthly numbers:

- Total Monthly Rent: $3,000 ($1,500 per unit)

- Mortgage (Principal & Interest): $2,022

- Property Taxes: $350

- Homeowners Insurance: $120

At first glance, this looks great! She has $3,000 coming in and $2,492 going out, leaving a tidy "profit" of $508. But this is the exact trap that sinks many new investors. We haven't accounted for the real costs of owning property.

Let's factor in the operating expenses Sarah absolutely must plan for:

- Vacancy Fund (5% of rent): $150 (for when a unit is empty between tenants)

- Repairs & Maintenance (8% of rent): $240 (for the inevitable leaky faucet or broken appliance)

- Capital Expenditures (CapEx) (7% of rent): $210 (to save for big-ticket items like a new roof or HVAC system)

- Property Management (10% of rent): $300 (even if she self-manages, her time is worth something!)

Now, let's run the numbers again with these crucial additions:

- Total Income: $3,000

- Total Expenses: $2,492 (PITI) + $900 (Operating Expenses) = $3,392

Suddenly, Sarah's "profitable" property has a negative cash flow of -$392 per month. This simple but thorough calculation just saved her from making a very expensive mistake. For a deeper dive into these calculations, check out our complete guide to analyzing rental property cash flow.

The Long-Term Wealth Builder: Appreciation

While cash flow keeps your investment healthy today, appreciation is what builds life-changing wealth tomorrow. It’s simply the increase in your property's value over time, and it comes in two main flavors.

- Market Appreciation: This is the value increase you get from external forces—things like inflation, job growth in the area, and more people moving in. You're basically getting a lift from a rising tide just by owning property in a good location.

- Forced Appreciation: This is the value you create. By renovating a dated kitchen, adding a bathroom, or dramatically improving the curb appeal, you can "force" the property's value to climb much faster than the rest of the market.

Ultimately, the best investments masterfully combine both. Cash flow gives you the financial stability to hold on for the long run, weathering any market ups and downs. Appreciation is the grand prize, delivering the massive equity growth that can become the cornerstone of your family's wealth for generations.

Smart Financing to Grow Your Portfolio

Let's talk about the single most powerful concept in real estate investing: leverage. This is the tool that separates the hobbyists from the serious wealth builders. At its core, leverage is simply using borrowed money—usually from a bank—to control a much larger asset.

Think about it. If you had to pay all cash for every property, building a portfolio would be a painfully slow process. Leverage changes the game completely.

By putting down a fraction of the property's cost, you get to benefit from 100% of its appreciation and cash flow. Your small investment punches way above its weight class. This is how savvy investors go from owning one door to dozens.

Foundational Financing Options

Before you get into the creative stuff, you need to master the basics. For most investors, the journey begins with one of two loan types.

A conventional loan is the workhorse of the industry. For a pure investment property, you’ll typically need a down payment of 20-25% and a good credit score. On the other hand, an FHA loan, which is insured by the government, opens the door for people with as little as 3.5% down. The catch? You have to live in the property.

This is exactly why so many new investors get their start with "house hacking"—using an FHA loan to buy a duplex or triplex, living in one unit, and having the tenants in the other units pay down their mortgage. It’s a brilliant way to get in the game with minimal cash out of pocket.

"Real estate investors understand that borrowing money can make sense for long-term investments. You might pay 6-7% interest rates on your mortgage while seeing 10-12% or more returns on that property, putting you solidly in the green."

Here’s a quick breakdown of how these two options stack up. Knowing how to finance an investment property is non-negotiable, and it starts here.

| Feature | Conventional Loan | FHA Loan |

|---|---|---|

| Minimum Down Payment | 20-25% for Investors | 3.5% |

| Occupancy Requirement | None for investors | Must live in the property |

| Best For | Acquiring a pure rental property from the start. | First-time investors using the "house hack" strategy. |

| Credit Score | Typically higher (620+, but 740+ for best rates) | More lenient (as low as 580) |

| Mortgage Insurance | Not required with 20%+ down | Required for the life of the loan |

Advanced Strategies for Scaling Your Portfolio

Once you’ve got a property or two under your belt, it's time to accelerate. Advanced financing strategies are all about acquiring more properties without waiting years to save up another 20% down payment.

One of the most popular and effective methods is the BRRRR method. It’s a five-step cycle that turns one investment into a repeatable system.

- Buy: Find a property that needs work and buy it below market value, often with short-term financing or cash.

- Rehab: Renovate the property to boost its value and make it attractive to tenants. This is called "forced appreciation."

- Rent: Get a quality tenant in place to create a stable income stream.

- Refinance: Go to a bank and get a new, long-term mortgage based on the property’s new, higher value.

- Repeat: The bank gives you cash back during the refinance. You then use that money as the down payment on your next property.

The BRRRR method is a true wealth-building engine. It lets you pull your initial capital back out and put it to work again and again, allowing you to scale your portfolio much faster than traditional methods.

Another great tool is seller financing. This is where the seller of the property essentially acts as your bank. You make payments directly to them instead of a traditional lender. It's a fantastic option if you can't get a conventional loan, and you can often negotiate more flexible terms, like a lower down payment. Finding a motivated seller is key, but this strategy can unlock deals you couldn't touch otherwise.

Mastering these financing tools is what separates a passive property owner from a strategic portfolio builder. It’s how you create a scalable system for generating long-term wealth.

How to Analyze Deals and Manage Risk

There’s a core principle every seasoned real estate investor lives by: you make your money when you buy, not just when you sell. Finding a genuinely good deal is more than a gut feeling. It’s about a clear-eyed analysis of the numbers and having a bulletproof plan for what could go wrong.

This is the moment you stop thinking like a homeowner and start acting like an investor. Learning to break down a property’s financial potential is hands-down the most important skill you can develop. It’s what separates a true opportunity from a money pit dressed up as a bargain.

The Essential Metrics for Sizing Up a Deal

Before an offer even crosses your mind, you need to run the numbers. A couple of key calculations give you a quick, yet powerful, snapshot of a deal's health: the Capitalization Rate (Cap Rate) and the Cash-on-Cash Return.

The Capitalization Rate, or Cap Rate, is all about the property's raw earning power. It measures the unleveraged annual return, telling you how hard the asset works on its own, completely separate from your loan. To find it, you simply divide the Net Operating Income (NOI) by the property’s price.

On the other hand, the Cash-on-Cash (CoC) Return is all about your specific investment. It looks at the annual cash flow you’ll pocket relative to the actual cash you put in—your down payment, closing costs, and upfront repair money. This metric shows the return on the money you personally have in the game.

Key Takeaway: A good Cap Rate signals a healthy property, but a great Cash-on-Cash Return signals a fantastic investment for you. You really need both to make a confident decision.

Comparing Key Deal Analysis Metrics

It’s crucial to get the difference between these two. One tells you about the property's built-in profitability, and the other tells you how efficiently you’re using your own capital.

| Metric | Calculation Formula | What It Tells You | Best For |

|---|---|---|---|

| Cap Rate | (Net Operating Income / Purchase Price) x 100 | The property's raw, unleveraged annual return. | Comparing the relative value of different properties across a market. |

| Cash-on-Cash Return | (Annual Cash Flow / Total Cash Invested) x 100 | The direct return on your personal cash investment. | Evaluating how well a specific deal works with your financing and cash. |

Running these numbers can feel a little intimidating at first, but it quickly becomes second nature. To make it easier and ensure you don’t forget any critical variables, you can plug the numbers into a dedicated real estate investment calculator.

The Due Diligence Checklist

The spreadsheet only tells part of the story. Once a property looks good on paper, it's time for due diligence—the deep-dive investigation where you verify every single one of your assumptions. This is your chance to uncover any hidden landmines before you’re legally committed.

Your due diligence should never skip these steps:

-

Professional Home Inspection: This is absolutely non-negotiable. A licensed inspector will crawl through the property's core systems—the foundation, roof, electrical, plumbing, and HVAC—to find potentially thousands of dollars in hidden defects.

-

Market Rent Analysis: Don't just take the seller's word for what the property rents for. Do your own homework. Check listings for comparable properties nearby. A sharp local real estate agent or property manager can be an invaluable source of truth here.

-

Reviewing Existing Leases: If tenants are already in place, you need to read their lease agreements with a fine-toothed comb. You're about to inherit these contracts, so you need to know the exact terms, rent amounts, and security deposit details.

Building Your Financial Safety Net

Even the most perfectly analyzed deal has risks. The secret to staying in the game long-term is to anticipate those risks and prepare for them. Smart investors always have a cushion.

Your main line of defense is a solid Capital Expenditures (CapEx) fund. This is just a separate savings account earmarked for the big, expensive, and infrequent replacements. Think a new roof ($8,000-$15,000), a new HVAC system ($5,000-$10,000), or other major projects. A good rule of thumb is to sock away 5-10% of the monthly rent just for this fund.

Beyond that, a rock-solid tenant screening process is your best defense against vacancies and missed payments. Always run background checks, pull credit reports, and verify income. Protecting your investment starts with putting the right people in your property—tenants who will care for it and pay their rent on time.

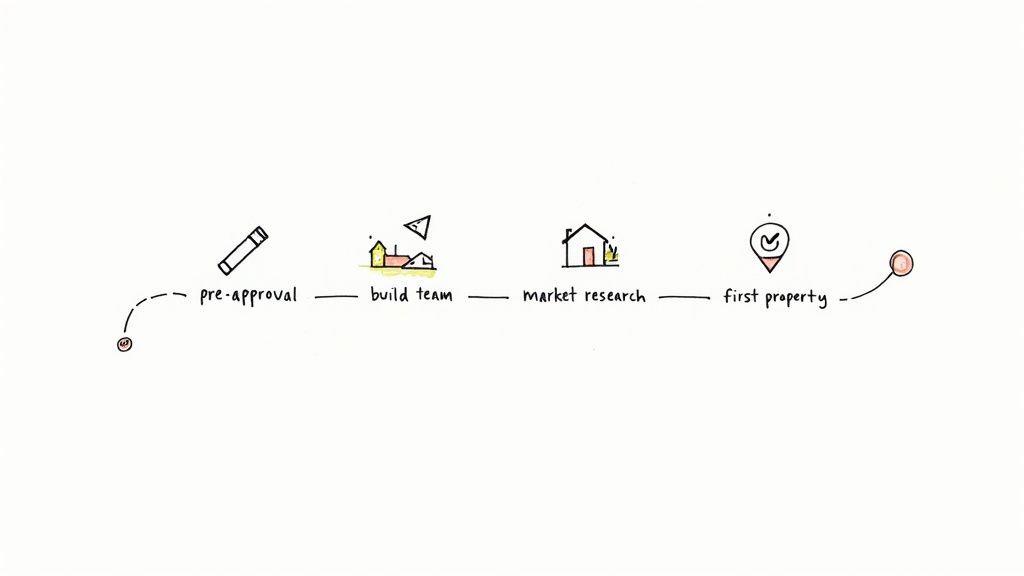

Your Action Plan for Getting Started

Alright, we’ve covered a ton of ground—from investment strategies to financing and running the numbers. But all the knowledge in the world doesn't build wealth. Action does. It's time to take what we've learned and turn it into a concrete game plan for getting you off the sidelines and into your first deal.

This is where the rubber meets the road.

Let's break down the process into clear, manageable phases. The idea here isn't to overwhelm you, but to give you a clear path to follow, one step at a time.

Phase 1: Prepare Your Finances

Before you even think about browsing listings on Zillow, you need to get your financial house in order. This is non-negotiable. Lenders are going to put your financial health under a microscope, so being prepared from day one will make everything else so much smoother.

Here's your checklist:

- Check Your Credit Score: This number is your golden ticket to better interest rates. You should be aiming for a score of 740 or higher if you want to unlock the most favorable loan terms.

- Calculate Your Debt-to-Income (DTI) Ratio: Lenders need to see that you can comfortably afford another mortgage payment. In their eyes, that usually means a DTI below 43%.

- Get Pre-Approved for a Loan: I can't stress this enough: a pre-approval is not the same as a pre-qualification. A real pre-approval means a lender has already dug into your finances and is willing to lend you a specific amount. This puts you in the driver's seat and makes your offers far more compelling to sellers.

Phase 2: Build Your Core Team

Let me be clear: real estate is not a solo sport. Trying to do it all yourself is a recipe for disaster. Assembling a small team of experts isn't a luxury—it's absolutely essential for making smart, protected investments.

- An Investor-Friendly Real Estate Agent: You don't just want any agent. You need someone who lives and breathes investment properties, understands the local rental market inside and out, and can analyze a deal like an investor, not just a homebuyer.

- A Responsive Mortgage Lender: Find a lender who has a deep well of experience with investment property loans. They'll be your guide through the maze of financing options, from conventional loans to more creative strategies.

- A Trusted Contractor and Inspector: Start building your list of reliable pros now, even before you buy. A great inspector will be your eyes on the ground, saving you from money pits, while a good contractor is worth their weight in gold when it's time for repairs or renovations.

"The difference between a successful real estate investor and a struggling one often comes down to the quality of their team. Surround yourself with experts who can see what you can't."

Phase 3: Identify and Analyze Your Market

With your financing lined up and your A-team in place, the hunt can finally begin. Remember, a successful investment is all about buying the right property in the right location.

Start by zeroing in on a few target neighborhoods. Look for strong fundamentals—things like job growth, good schools, and low crime rates. Then, get in your car and drive through these areas. Get a feel for the community.

Once you're familiar with the turf, you can start analyzing deals as they hit the market. This is where you put our earlier lessons to work. Run the numbers using the cash-on-cash and cap rate formulas for every single property that catches your eye.

This methodical approach takes the emotion out of the decision-making process. It turns what feels like a huge, intimidating journey into a series of clear, logical steps.

Frequently Asked Questions (FAQ)

Here are answers to the 10 most common questions aspiring real estate investors ask.

1. How much money do I really need to start investing in real estate?

This depends entirely on your strategy. For a traditional rental, you'll need 20-25% down. However, you can use an FHA loan for a multi-family property you live in ("house hacking") for as little as 3.5% down. For a completely passive approach, you can invest in Real Estate Investment Trusts (REITs) with just a few hundred dollars.

2. Is real estate still a good investment with high interest rates?

Yes, but your strategy must adapt. High rates increase mortgage costs, squeezing cash flow. However, they also reduce buyer competition, creating opportunities to negotiate better purchase prices. Successful investors in this environment focus on properties in high-demand rental markets and plan to refinance when rates eventually decrease.

3. What is the single biggest mistake new investors make?

The most common and costly mistake is underestimating expenses. New investors often focus only on the mortgage payment and forget about property taxes, insurance, maintenance, vacancy periods, and capital expenditures (like a new roof or HVAC system). A deal that looks profitable on paper can quickly become a money-loser without a comprehensive budget.

4. Do I need to be an expert in construction to flip a house?

No. Your role is to be the project manager, not the carpenter. Your success depends on building a reliable team, including a thorough home inspector to identify issues before you buy and trustworthy contractors to perform the renovation work on time and on budget.

5. What is "house hacking" and is it a good way to start?

House hacking is an excellent entry-level strategy. It involves buying a multi-unit property (like a duplex or triplex), living in one unit, and renting out the others. The rental income from your tenants can significantly offset or even cover your entire mortgage payment. It's powerful because it allows you to qualify for owner-occupant loans with much lower down payments.

6. How do you find good, reliable tenants?

You don't find good tenants by luck; you find them through a rigorous and consistent screening process. This process should include a background check, credit report analysis, income and employment verification, and calls to previous landlords for references. A standardized system is your best defense against future problems.

7. Should I hire a property manager?

It depends on your goals. If you desire a passive investment, live far from your property, or don't want to handle day-to-day management tasks, a property manager is essential. They typically charge 8-10% of the monthly rent but save you significant time and stress by handling tenant screening, rent collection, and maintenance calls.

8. What is the difference between cash flow and appreciation?

Think of it this way: Cash flow is the profit you have left each month after collecting rent and paying all expenses. It's your immediate, predictable income. Appreciation is the long-term increase in the property's value over time. Positive cash flow is critical because it allows you to hold the asset long enough to benefit from significant appreciation.

9. How many properties do I need to own to retire?

There is no magic number. The answer depends on your "financial freedom number"—the annual income you need to live your desired lifestyle in retirement. Once you determine that number, you can calculate how many cash-flowing rental properties you need to acquire to generate that income stream.

10. What is the BRRRR method?

BRRRR is an acronym for a powerful real estate investing strategy: Buy, Rehab, Rent, Refinance, Repeat. The process involves buying an undervalued property, renovating it to increase its value ("force appreciation"), renting it to a tenant, and then doing a cash-out refinance to pull your initial investment capital back out. You then use that capital to Repeat the process on a new property, allowing for rapid portfolio growth.

This article is for educational purposes only and is not financial or investment advice. Consult a professional before making financial decisions.

At Top Wealth Guide, we provide the insights and strategies you need to navigate the complexities of financial markets and build a secure future. Explore our resources to enhance your investment portfolio. https://topwealthguide.com