The investment decision making process shouldn't start with chasing the latest hot stock tip. It's a structured journey that begins with a clear understanding of your personal financial landscape. Before you put a single dollar to work, you need to map out what you want to achieve, how much risk you can stomach, and the rules you'll follow to get there.

In This Guide

- 1 Building Your Personal Investment Framework

- 2 How to Research and Analyze Investment Opportunities

- 3 Valuation Techniques That Actually Work

- 4 How to Manage Risk and Build Your Portfolio

- 5 Executing, Monitoring, and Rebalancing Your Portfolio

- 6 Frequently Asked Questions About the Investment Decision Making Process

- 6.1 1. How often should I check my investment portfolio?

- 6.2 2. What's the biggest mistake beginners make in their investment process?

- 6.3 3. How do I determine my personal risk tolerance?

- 6.4 4. Should I change my strategy based on market news?

- 6.5 5. What is the real difference between investing and speculating?

- 6.6 6. Is it better to invest a lump sum or use dollar-cost averaging?

- 6.7 7. How many stocks should I own for proper diversification?

- 6.8 8. Why do I need an "investment thesis" for each investment?

- 6.9 9. When is the right time to sell an investment?

- 6.10 10. How can I incorporate ESG factors into my decision-making?

Building Your Personal Investment Framework

Think of your investment framework as your personal financial constitution. It’s the set of principles that keeps you grounded when the market inevitably gets choppy. Without it, it’s all too easy to let fear or greed take the wheel, making reactive choices that can sabotage your long-term plans.

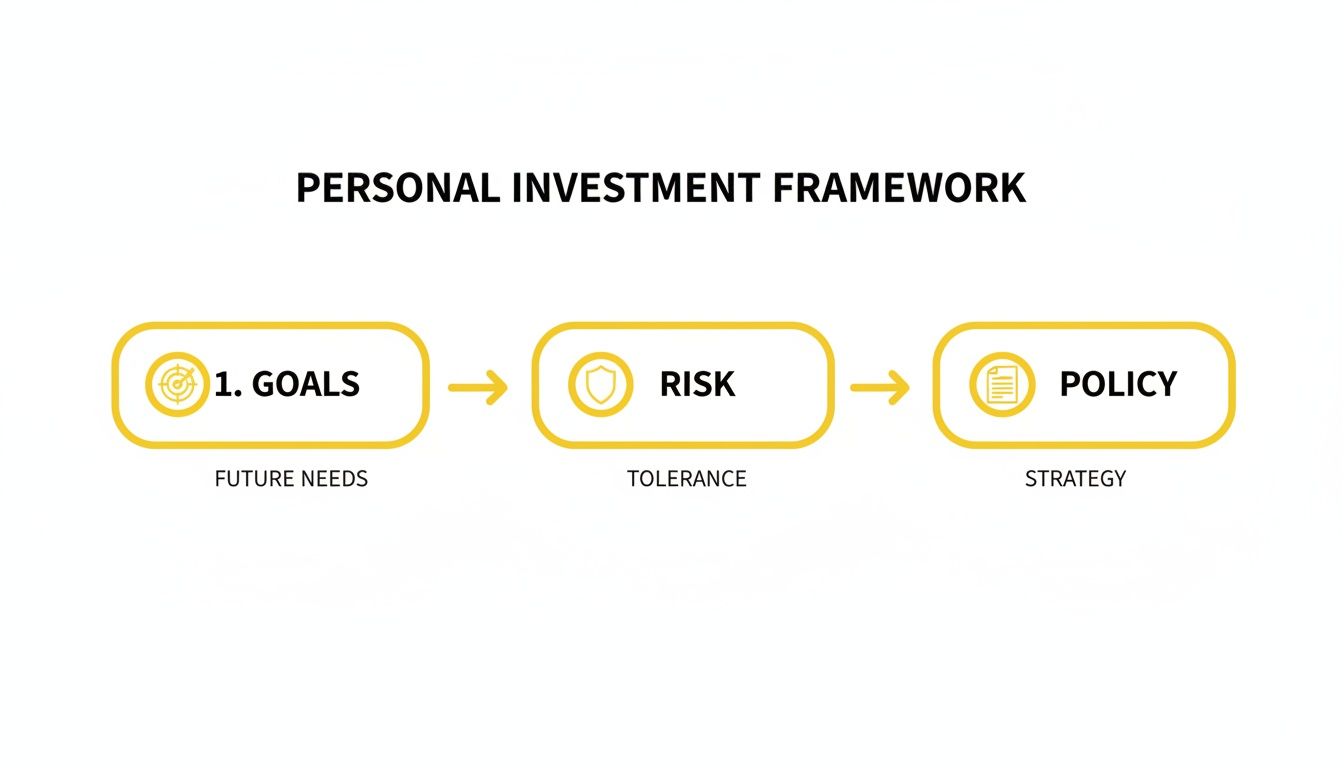

This foundation rests on three crucial pillars: getting crystal clear on your goals, being brutally honest about your risk tolerance, and codifying it all in a formal Investment Policy Statement (IPS).

Define Your Financial Goals

Saying you want to "save for the future" is a nice thought, but it's not an actionable plan. To build a strategy that works, you must get specific. Are you saving for a down payment on a house in five years? Or are you funding a retirement that's thirty years away? The answer drastically changes the kinds of investments that make sense for you.

A truly actionable goal is a SMART one:

- Specific: Nail down exactly what you're aiming for (e.g., "a $50,000 down payment for a house").

- Measurable: Put a number on it so you can track your progress.

- Achievable: Ensure it’s realistic for your income and savings habits.

- Relevant: It must align with your life's bigger picture.

- Time-Bound: Give yourself a deadline (e.g., "in five years").

For a deeper dive, our guide on how to set SMART financial goals can help you lay this groundwork properly.

Assess Your Real Risk Tolerance

It’s one thing to say you're comfortable with risk on a questionnaire. It's another thing entirely to live through a major market downturn. You have to ask yourself honestly: how would you really feel if your portfolio suddenly dropped 20% or 30%? Would you panic and sell everything, or would you see it as a chance to buy more at a discount? Your gut reaction is just as important as your financial ability to absorb a loss.

This is where you move from abstract ideas to a concrete plan, connecting your future needs with your comfort level for risk to create a guiding strategy.

This simple flow shows that a solid strategy isn't a random guess; it's a logical path forward that creates a stable foundation for every decision you'll make.

Create Your Investment Policy Statement

Your Investment Policy Statement (IPS) is your personal rulebook for investing. It's a written document that clearly lays out your goals, your risk tolerance, and the strategies you'll use to hit those targets.

An IPS is your best defense against your own worst instincts. When markets are going haywire, this document is what you pull out to remind yourself of the long-term plan, stopping you from panic-selling at the bottom or chasing hype at the top.

Even the biggest players navigate tricky environments. Consider that global foreign direct investment recently fell by 11% to $1.5 trillion. This shows that large institutional investors are also adjusting to major headwinds like inflation (a concern for 44% of investors) and geopolitical tensions (42%).

Interestingly, in this uncertain climate, investors are concentrating their capital, with a whopping 67% identifying the United States as the most attractive market. This suggests a broader "flight to safety" and perceived growth. Understanding these big-picture trends can give you valuable context for your own strategy.

How to Research and Analyze Investment Opportunities

Once you’ve built your personal investment framework, it's time to get into the nitty-gritty. This is where you move from planning to action, putting on your detective hat to vet potential investments and see if they actually fit your strategy.

Having a structured, repeatable research process is your best defense against market noise and emotional decision-making. It’s what separates disciplined investors from speculators. The goal is to blend two key disciplines: fundamental analysis, which is all about figuring out an asset's intrinsic value, and technical analysis, which involves studying charts and market trends. Mastering both gives you a much clearer picture of what you're buying.

Analyzing Traditional Stocks

When you're looking at stocks, you're not just buying a ticker symbol; you're buying a piece of a business. Your first job is to understand that business inside and out. How healthy is it? What makes it better than its competitors? What are its growth prospects?

The best place to start is with the company's financial statements. The balance sheet, income statement, and cash flow statement are the bedrock of your research. If you need a refresher, our guide on how to analyze financial statements breaks it all down.

From there, calculating a few key financial ratios can give you a quick snapshot of the company's performance. These are some of my go-tos:

- Price-to-Earnings (P/E) Ratio: This classic metric compares the stock price to its earnings per share. A sky-high P/E might mean the stock is overhyped, while a low one could signal a potential bargain.

- Debt-to-Equity Ratio: This shows you how much debt a company is using to finance its operations. A high ratio isn't always bad, but it can be a red flag, indicating higher risk.

- Return on Equity (ROE): This is a powerful measure of profitability. It tells you how well the company's management is using shareholders' money to generate profits. Consistently high ROE is often the mark of a quality business.

Remember, no single metric tells the whole story. The power comes from using these ratios together to build a complete picture of a company's strengths and weaknesses relative to its competitors.

Vetting Real Estate Investments

Analyzing real estate is a different beast. Here, it’s all about the property's potential to put cash in your pocket. While you're dealing with a physical asset, the financial due diligence is just as crucial.

Your focus should be squarely on cash flow and return. I always start with two core calculations for any potential rental property:

- Capitalization (Cap) Rate: This is your Net Operating Income (NOI) divided by the property's market value. It's a fantastic way to compare the potential returns of different properties on an apples-to-apples basis.

- Cash-on-Cash Return: This metric is more personal. It measures the annual cash flow you receive against the actual cash you invested out-of-pocket. It shows you exactly what your money is earning you.

Real-Life Example: Comparing Two Rental Properties

Imagine you are considering two different rental properties. Property A costs $300,000 and generates $24,000 in annual net operating income (NOI). Property B costs $450,000 and generates $30,000 in NOI.

| Metric | Property A | Property B | Analysis |

|---|---|---|---|

| Price | $300,000 | $450,000 | – |

| NOI | $24,000 | $30,000 | – |

| Cap Rate (NOI/Price) | 8.0% | 6.7% | Property A offers a better return for every dollar of its value. |

| Down Payment (20%) | $60,000 | $90,000 | – |

| Cash-on-Cash Return | 40% ($24k/$60k) | 33% ($30k/$90k) | Property A also provides a higher return on the actual cash invested. |

Based on these key metrics, Property A appears to be the superior investment, even though it's the cheaper property. This demonstrates why a structured analysis is vital.

Valuation Techniques That Actually Work

Here’s one of the most important lessons in investing: price is what you pay, but value is what you get. Confusing the two is a surefire way to overpay for an asset and sabotage your returns from the start.

Learning how to properly value an investment is a game-changer. It’s what separates speculators from serious investors and transforms your entire investment decision making process.

The trick is knowing that you can't use the same yardstick for every asset. The tools that work for a blue-chip stock are completely useless for a rental property. The real skill is matching the right valuation technique to the right asset class.

Finding the Fair Value of Stocks

When it comes to stocks, valuation boils down to two main approaches: absolute valuation (what a company is worth on its own merits) and relative valuation (how it stacks up against its peers).

The Discounted Cash Flow (DCF) model is the heavyweight champion of absolute valuation. It’s a detailed process where you forecast a company's future cash flows and discount them back to today's dollars to find its intrinsic value. It gives you a solid, fundamentals-based number to anchor your analysis. We dive much deeper into this in our full guide on how to value stocks.

For a quicker take, you can turn to relative valuation. This involves using simple ratios like Price-to-Earnings (P/E) or Price-to-Sales (P/S) to compare a company to its competitors or its own historical performance.

Pro Tip: Don't just pick one. I always start with a DCF analysis to build my conviction in a company's fundamental worth. Then, I use relative metrics like the P/E ratio as a sanity check to see how the market is currently pricing it. The combination is powerful.

Appraising Real Estate Properties

Real estate plays by a different set of rules. Here, valuation is all about the physical property and its ability to generate income. Investors lean on three core methods:

- Sales Comparison Approach: This is your bread and butter for residential properties. You simply look at the recent sale prices of similar homes ("comps") in the same neighborhood to get a reliable benchmark.

- Income Approach: If you're buying a rental, this is non-negotiable. This method values a property based on its income stream, using its Net Operating Income (NOI) and a capitalization (cap) rate.

- Cost Approach: This determines value by figuring out what it would cost to build the exact same property from the ground up, factoring in land and construction costs minus any depreciation. It's most useful for unique properties or new construction.

Valuing New-Age Digital Assets

Valuing assets like cryptocurrencies is tough. They don't have cash flows, which makes traditional models useless. Instead, analysts have developed unique metrics to gauge the health and adoption of a network.

One of the most interesting is the Network Value to Transactions (NVT) ratio. Think of it as a sort of "P/E ratio for crypto." It compares a crypto's total market cap to the dollar value of transactions running through its network. A sky-high NVT ratio could be a red flag, suggesting its price has gotten way ahead of its actual usage.

Understanding new digital assets is critical. Technology is now a dominant force, with 61% of investors believing it's the most likely sector to attract capital in the next three years. Specifically, AI and generative AI are pulling in massive amounts of cash—$33.9 billion in private investment alone. For smart investors, this is a clear signal: aligning with these major capital flows could be a profitable long-term strategy. You can read more about what's on investors' minds at pwc.com.

Comparison of Valuation Methods by Asset Class

To simplify, this table breaks down which valuation methods work best for each asset class. This helps you pick the right tool for the job every time.

| Valuation Method | Asset Class | Key Metric(s) | Best For | Potential Pitfalls |

|---|---|---|---|---|

| Discounted Cash Flow (DCF) | Stocks | Future Cash Flow, Discount Rate | Stable, predictable businesses | Highly sensitive to assumptions |

| Relative Valuation (P/E, P/S) | Stocks | P/E Ratio, P/S Ratio, EV/EBITDA | Quick comparisons within an industry | The entire market can be overvalued |

| Sales Comparison Approach | Real Estate | Price of Comparable Properties | Residential homes, condos | Finding truly identical "comps" is hard |

| Income Approach | Real Estate | Net Operating Income, Cap Rate | Commercial and rental properties | Relies on accurate income forecasts |

| Network Value to Transactions (NVT) | Cryptocurrency | Market Cap, Transaction Volume | Assessing network utility and adoption | Still an evolving and unproven metric |

Choosing the right valuation method isn't just an academic exercise—it's a crucial step that directly impacts your returns.

How to Manage Risk and Build Your Portfolio

Finding a promising investment is only half the equation. The real secret to long-term wealth lies in protecting your capital and building a portfolio that can weather any storm. This is the defensive game, the discipline that separates a lucky break from sustainable success.

It’s about more than just picking a few different stocks. True portfolio construction is about strategically blending assets that react differently to economic shifts. This means looking beyond just stocks and bonds to diversify across different countries and industries.

The Art of Sizing Your Bets

One of the most important questions you'll ask is: how much money should I put into a single idea? This is position sizing, and it forces you to confront the potential downside before dreaming of the upside.

A great rule of thumb, used by seasoned investors, is the 1% rule. The principle is simple: never risk more than 1% of your total investment capital on any single position. If you have a $100,000 portfolio, this means your maximum loss on any one investment is capped at $1,000.

This isn't about capping your profits; it's about ensuring you can survive a losing streak. The 1% rule ensures that a few bad calls won't knock you out of the game, giving you time for your winning ideas to shine.

Practical Tools to Protect Your Capital

Beyond smart position sizing, you can use a few tactical tools to shield your portfolio when markets get choppy. Think of them as your automated safety nets.

- Stop-Loss Orders: This is a simple instruction for your broker to sell a stock if it falls to a specific price. It’s your pre-planned exit strategy, putting a hard cap on how much you can lose.

- Hedging Techniques: For more experienced investors, options can be a powerful hedging tool. For example, buying put options on a major market index like the S&P 500 can act as insurance for your portfolio, since their value typically rises when the overall market falls.

A well-structured portfolio is always your best defense. For a much deeper dive into this, check out our guide on how to optimize your portfolio with smart asset allocation.

Diversify with an Eye on Growth

Building a tough portfolio also means finding opportunities in sectors with powerful, long-lasting growth trends. A perfect example right now is the explosive demand for data centers, driven by the rise of artificial intelligence.

This isn't just a small trend; big money is flooding in. A recent survey from CBRE found that 95% of major investors are planning to increase their data center investments. What's more, 41% are putting $500 million or more to work in this space, up from just 30% last year. This major shift shows just how massive the computational needs of AI are, creating a fantastic opportunity for individual investors through specialized REITs or infrastructure funds.

Executing, Monitoring, and Rebalancing Your Portfolio

You’ve done the hard work of researching and building a portfolio you believe in. But the investment decision making process doesn't end when you click "buy." In many ways, it's just getting started.

This is the ongoing cycle of executing your trades, keeping an eye on your holdings, and making smart, disciplined adjustments. It all starts with how you actually place an order.

Getting the Best Price: A Crash Course in Order Types

Simply hitting "buy" isn't the whole story. The type of order you place can mean the difference between getting the price you want and getting a nasty surprise. Let’s break down the three essential orders.

| Order Type | What It Does | My Rule of Thumb for Using It |

|---|---|---|

| Market Order | Buys or sells an asset instantly at the best available price. | Use this only when speed is your top priority. It's best for highly liquid stocks or ETFs where the price isn't moving wildly. |

| Limit Order | Lets you set a specific price (or better) for your trade. | This is my go-to for most trades. It puts you in control, ensuring you don’t overpay for an asset or sell it for less than you’re comfortable with. |

| Stop Order | Becomes a market order once a specific price is hit. A stop-loss is set below the current price to limit losses. | Think of this as your automated risk-management tool. A stop-loss takes the emotion out of selling a losing position. |

The Discipline of Watching Your Portfolio

With your investments in place, it’s time to monitor them. This doesn’t mean gluing your eyes to the screen and agonizing over every daily fluctuation—that’s a recipe for anxiety.

Instead, think of it as a scheduled health check-up. I personally put a recurring reminder on my calendar to review my portfolio every quarter. A semi-annual review works well, too.

During this check-in, I run through a quick mental checklist:

- Asset Allocation: Has one position grown so much that it's throwing my target percentages out of whack?

- Performance vs. Thesis: Are my investments behaving the way I expected? If not, why?

- Life Goals: Have any of my financial goals or timelines shifted?

This approach keeps you connected to your strategy without getting lost in the noise.

Rebalancing: The Closest Thing to a Free Lunch in Investing

Over time, your portfolio will naturally drift. Your winners will become a larger slice of the pie, while the laggards shrink. Rebalancing is the simple—yet incredibly powerful—act of trimming your winners and buying more of your underperformers to get back to your original target allocation.

In practice, rebalancing forces you to do what every smart investor knows they should but often lacks the discipline for: systematically selling high and buying low. You’re taking profits off the table and reinvesting them into assets that are now comparatively cheaper.

This isn’t just about tidying up; it actively manages risk by preventing you from becoming overexposed to an asset that has run up in price. It's one of the most effective, rules-based ways to keep your portfolio healthy for the long haul. To dive deeper, you can explore various portfolio rebalancing strategies in our guide.

Frequently Asked Questions About the Investment Decision Making Process

1. How often should I check my investment portfolio?

For most long-term investors, a quarterly or semi-annual review is sufficient. This frequency allows you to stay on top of your asset allocation without reacting emotionally to short-term market noise. The goal is to review, not to constantly trade.

2. What's the biggest mistake beginners make in their investment process?

The most common and costly mistake is letting emotions drive decisions. This often manifests as panic selling during market downturns or FOMO (fear of missing out) buying into assets at their peak. A written Investment Policy Statement (IPS) is the best defense against emotional reactions.

3. How do I determine my personal risk tolerance?

Risk tolerance is a combination of your financial ability and emotional comfort with potential losses. Consider factors like your age, income stability, and investment timeline. Then, perform a gut check: could you sleep at night if your portfolio dropped 20%? An honest answer is crucial for building a sustainable strategy.

4. Should I change my strategy based on market news?

Generally, no. A robust investment strategy is designed for the long term and should not be altered based on daily headlines or pundit predictions. Making frequent changes often leads to poor timing and higher transaction costs. Stick to your plan unless there's a fundamental change in your financial situation or long-term goals.

5. What is the real difference between investing and speculating?

Investing is the process of allocating capital to an asset with the expectation of generating income or appreciation over a long period, based on fundamental analysis. Speculating involves taking on significant risk in the hope of making a large profit from short-term price fluctuations, often driven by market sentiment rather than intrinsic value.

6. Is it better to invest a lump sum or use dollar-cost averaging?

Historically, lump-sum investing has often yielded higher returns because markets tend to rise over time. However, dollar-cost averaging (investing a fixed amount regularly) is an excellent strategy for reducing risk and removing emotion from the timing of your investments. For most people investing from their income, it's the most practical approach.

7. How many stocks should I own for proper diversification?

While there is no magic number, holding 20-30 individual stocks across various uncorrelated sectors is often cited as a good benchmark for achieving adequate diversification. For a simpler approach, a few broad-market index funds or ETFs can provide instant diversification across thousands of companies.

8. Why do I need an "investment thesis" for each investment?

An investment thesis is your documented reason for buying a particular asset. It outlines what you expect to happen and why. This thesis acts as an objective benchmark. If the core reasons for your investment no longer hold true, it provides a rational basis for selling, preventing you from holding on to a losing position for emotional reasons.

9. When is the right time to sell an investment?

You should have a selling plan before you buy. Common reasons to sell include: your original investment thesis is no longer valid, the asset has become significantly overvalued, the position has grown too large and unbalances your portfolio, or you have identified a demonstrably better investment opportunity.

10. How can I incorporate ESG factors into my decision-making?

You can integrate Environmental, Social, and Governance (ESG) criteria by using negative screening (excluding industries like tobacco or fossil fuels) or positive screening (actively seeking out companies that are leaders in ESG practices). The simplest method is to invest in specific ESG-focused mutual funds or ETFs that handle the research and screening for you.

Ready to take control of your financial future? At Top Wealth Guide, we provide the insights and strategies you need to build and manage your wealth effectively. Explore our resources and start making smarter investment decisions today at https://topwealthguide.com.

This article is for educational purposes only and is not financial or investment advice. Consult a professional before making financial decisions.