Most Americans are living on a razor’s edge — one paycheck away from financial calamity. When the unexpected hits (and it will), they’re reaching for credit cards like life rafts. Problem is, these “life rafts” come with high interest and years of repayment… more like a weight chained to your ankle than a floatation device.

Enter: The Emergency Fund. This is the game-changer. At Top Wealth Guide, we’ll tell you… stashing away a little cash is like a financial vaccine. It protects you from those nasty surprises life loves to lob at you and keeps your anxiety levels in check. Peace of mind in a savings account — that’s the real wealth.

In This Guide

What Exactly Is an Emergency Fund

Picture this: an emergency fund is that chunk of cash chilling in your savings account, ready to tackle life’s oh-no moments without dragging you into the debt abyss. We’re talking car repairs that pop out of nowhere, that out-of-the-blue pink slip, or those pesky medical bills that decide to show up uninvited. This pile of cash isn’t mingling with your checking account or chasing the stock market’s ups and downs – nope, it’s not for that dreamy vacation or the latest iGadget.

The Harsh Reality of American Emergency Savings

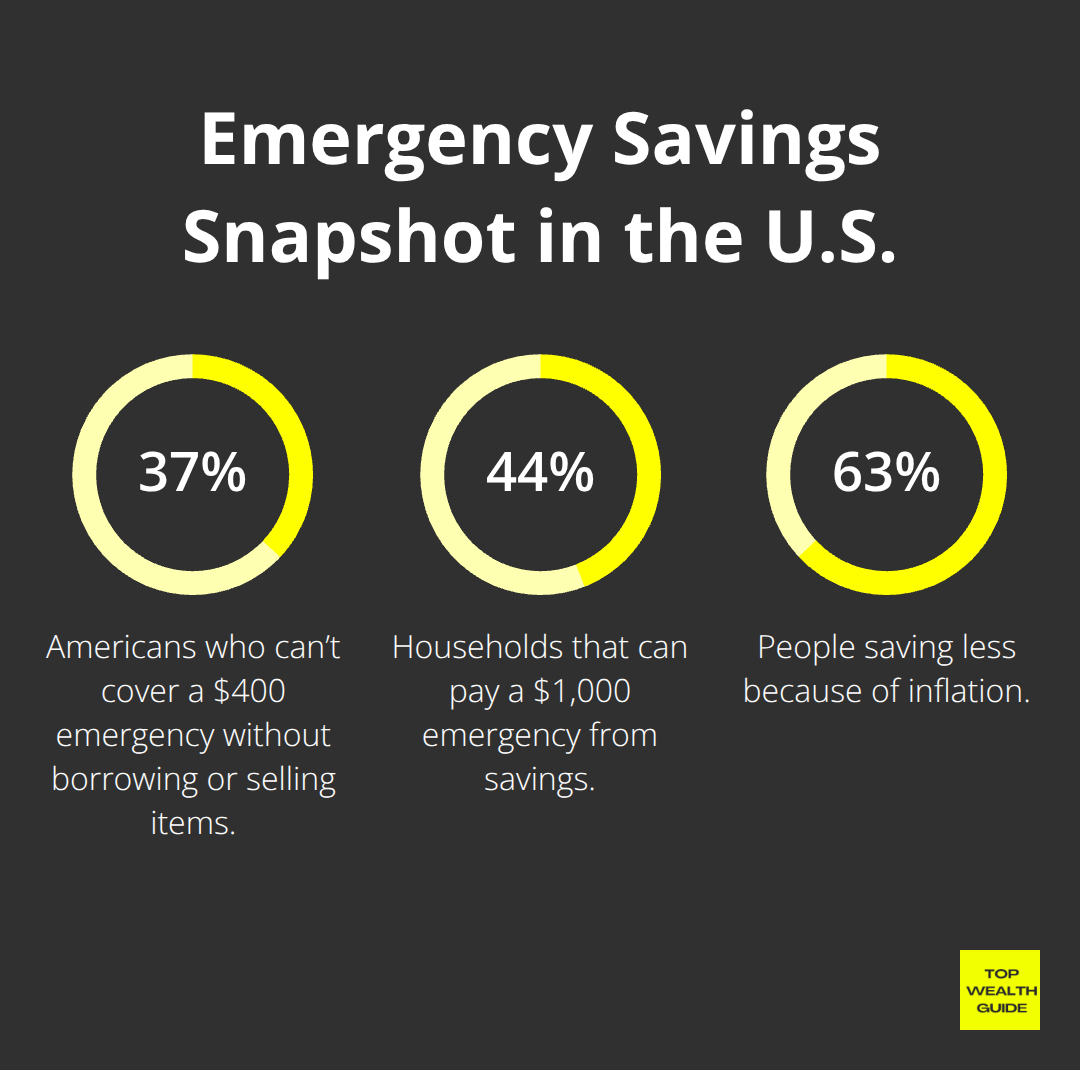

Here’s the brutal truth (brace yourself) – 37% of Americans don’t have $400 for an emergency without resorting to borrowing or pawning off something. And Bankrate’s 2024 survey?

Yeah, it paints a bleak picture where just 44% can swing a $1,000 emergency from their savings, whereas a staggering 63% are saving less thanks to the joy of inflation. These numbers? They’re screaming out the financial fragility that’s taken hold in households coast to coast.

When Emergency Funds Save the Day

Here’s the thing – real emergencies? They swoop in and clean out those bank accounts pronto. Lose your job, and you’re suddenly the finance minister in charge of rent, groceries, and utilities – all while job hunting becomes your full-time gig. Medical chaos? Boom, you’re signing checks with more zeroes than you’d like, even if you have insurance. Home woes like roof leaks or furnace meltdowns? They don’t wait for payday. And if the trusty car decides to quit, you’re left-side-of-the-road-stranded, figuring out how to get to work.

The Cost of Not Having Emergency Savings

No emergency stash? That’s where the trouble really brews. Families have to juggle choices like high-interest credit cards, payday loans, or – gasp – raiding retirement accounts. And those are expensive blunders with long-haul financial repercussions. Credit card rates? They’re rocking an average of 24% annually (turning a $5,000 emergency into a shocking $6,200 after a year). Payday loans? They laugh at a mere 400% APR. While 401(k) loans – they might as well be financial landmines, triggering taxes and penalties if you can’t pay them back on time.

So, the million-dollar question isn’t if you’ll face an emergency – but how big of a wad of cash you’ll need when life’s curveball comes hurtling your way.

How Much Cash Do You Actually Need

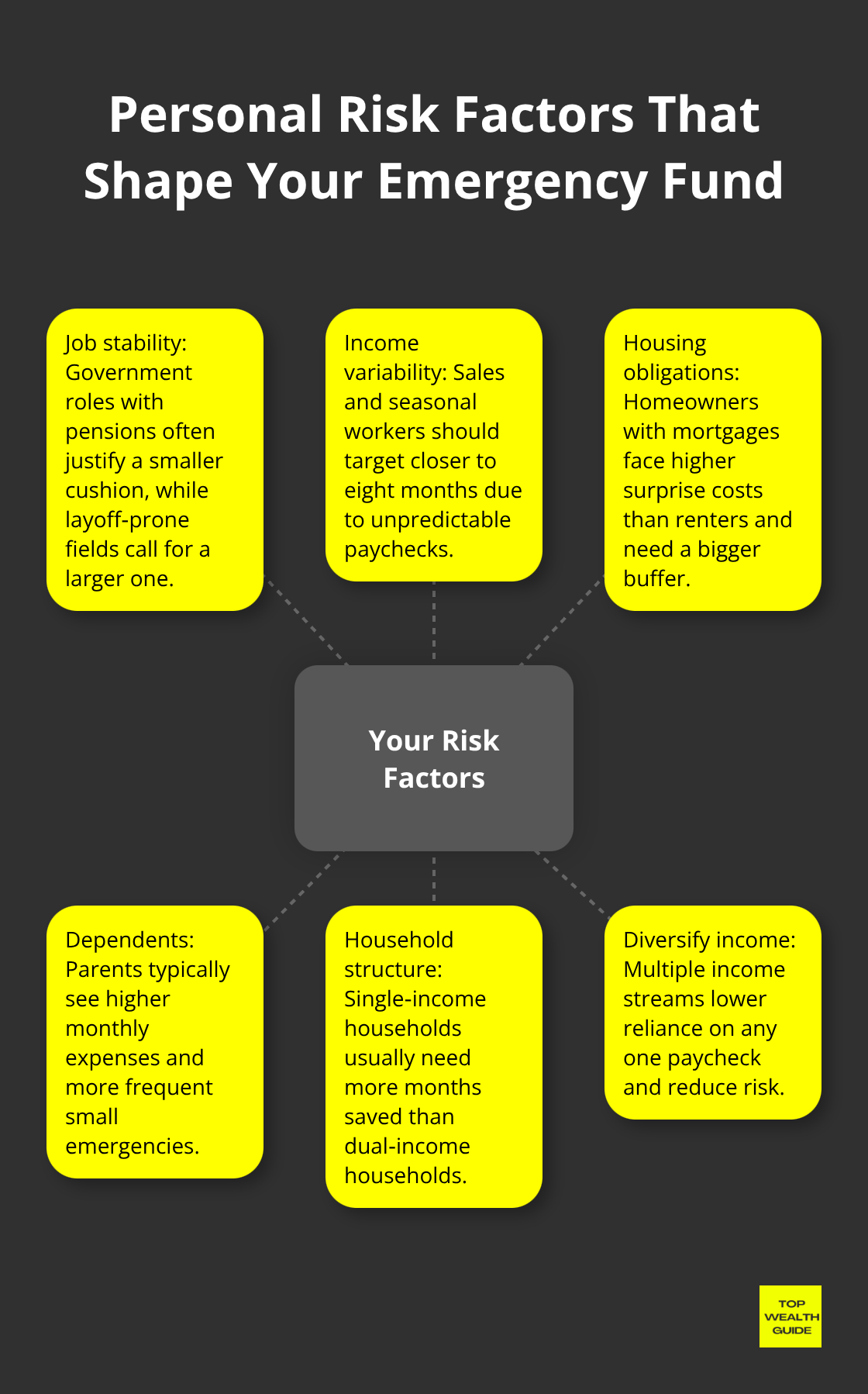

So, everyone’s heard it, right? The ol’ “save three to six months of expenses” mantra. But – shocker – most folks flub it. They either go bust when life throws a curveball or they’re stuck hoarding loads of cash that just, well, lounges around doing zilch. Your cash stash size? Totally riding on job stability, family headcount, and those pesky monthly bills. Got a single income and a couple of kiddos? Don’t even think less than six months. Duo incomes, no kids, stable gigs? Three months could maybe cut it. Freelancers and commission warriors? Aim for closer to eight months ‘cause your paycheck tango is unpredictable.

Calculate Your Real Monthly Expenses

Skip the guess games – track every cent for three months. We’re talking housing, utilities, food, insurance, those minimal debt dues, transport… the whole nine yards. Slam these essentials together and multiply by your “oh-crap” months number. Spending $4,500 a month just to keep the lights on? You’re staring at $13,500 for three months or a whopping $27,000 for six. Oh, and you’re probably off by about 20% since weird expenses like car tags or yearly insurance bills get left out in the cold.

Start Small and Build Smart

Forget about staring down that monster target sum. Start with $1,000 – beats the tiny emergencies without torpedoing your wallet. Fun fact: 73 percent of folks are barely saving for emergencies thanks to inflation deciding to act out. Once you hit $1,000, shoot for one month’s outlay, then slowly stack up to your ultimate goal. Key? Consistency. Even $50 a week sneaks you $2,600 a year, and that milestone sneaks up faster than you’d guess. Aiming higher? Same rules, tougher targets.

Adjust Based on Your Risk Factors

Your scenario dictates if the cookie-cutter advice is your best friend or your worst enemy. Government gig with pensions? Three months is cozy (job security, anyone?). Sales hotshots or those bouncing with the seasons should be eyeing eight months. Why? Income rollercoasters.

Got a mortgage instead of a lease? More cash – you’re your own landlord, buddy. Parents with kids? Bigger bills, more mini crises. Alone? Not so much. And hey, maybe think about diversifying those income streams, so you’re not clinging to a solo paycheck.

Now that you’ve pinned down that magic number, the million-dollar query is: where do you stash it? It’s gotta be safe but ready to jump when stuff goes sideways.

Where Should You Park Your Emergency Cash

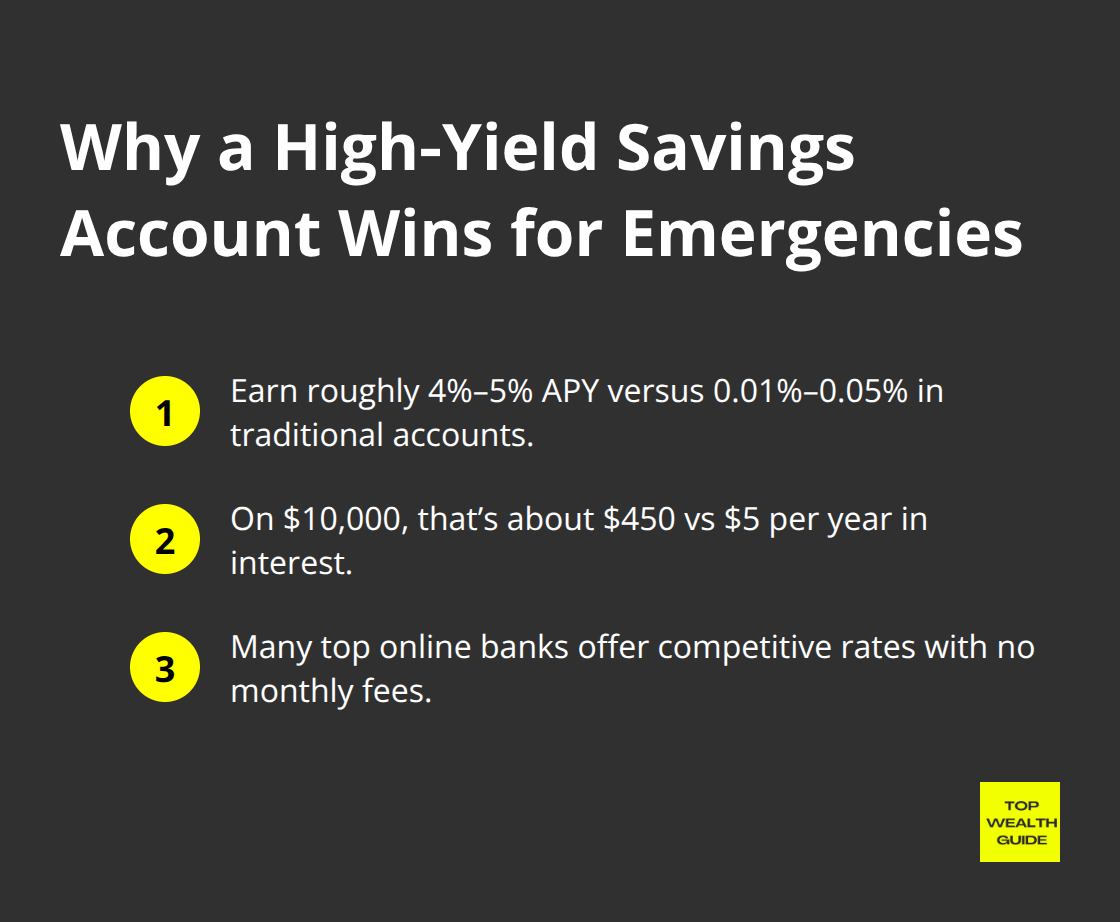

High-yield savings accounts are the rock stars of emergency funds-nothing else even comes close. These accounts offer interest rates in the range of 4% to 5% these days (late 2024), while traditional savings accounts barely make a whimper at 0.01% to 0.05%. Names like Marcus by Goldman Sachs, Ally Bank, and Capital One 360 are dropping serious value bombs with competitive rates and zero monthly fees.

Do the math: drop $10,000 into a traditional savings account, and you might earn a sad $5 a year-seriously. Or, go high-yield and scoop up $450 instead. That extra $445? That’s your car repair fund without scratching the main stash.

Money Market Accounts Offer Extra Flexibility

Money market accounts are the bridge you didn’t know you needed-between savings and checking accounts. They give you higher interest rates than your average savings account plus a sprinkling of check-writing privileges. Schwab Bank and Fidelity are solid players here, throwing in debit cards for those gotta-have-it-now emergencies. The catch? You need to have some skin in the game-think minimum balances of $1,000 to $10,000. Best play these cards when you’ve beefed up your emergency fund and want smoother access without slashing the yield too much.

Traditional Checking Accounts Fail the Test

Here’s the thing with checking accounts-they’re the villains in the emergency fund story. Paying next to nothing and opening the trapdoor to impulse buys. Most checking accounts dangle interest rates under 0.1% (which is pretty much zero when it comes to your emergency savings). Sure, they’re convenient for daily spendings, but when it comes to emergency funds, you need barriers. Real ones. Between your money and those everyday spending temptations.

Investments Create Dangerous Volatility

Investments are the wild card you don’t want in your emergency fund deck. Remember when the S&P 500 nosedived 21% in the first half of 2022? Or when Bitcoin took a 65% plunge? Imagine losing your job during a market slump and watching your buffer plummet by 30%. Not cool. CDs and Treasury bills? They’ll lock in your cash for months or years-missing the whole point of fast access. Your emergency fund craves the snooze fest of predictability, not the drama of the market. FDIC-insured savings accounts are the heroes-keeping your money safe and on a steady growth path, minus the roller coaster ride.

Final Thoughts

An emergency fund-it’s like giving your financial life a serious upgrade from reactive to proactive. Picture this… you’re handling emergencies with the grace of a ballerina, zero debt dance involved, instead of that gut-wrenching scramble for credit cards when life’s curveballs hit. The peace of mind? Priceless. Seriously, every dollar stashed away is worth its weight in gold.

So, start today… yes, just start. Whatever amount you can swing. Open up a high-yield savings account-automate those transfers like you’re setting up a Netflix subscription. $25, $50, $100 weekly (check the progress each month, maybe even throw a mini-celebration for each milestone). In a few months, voila-you’ve got yourself a financial cushion that’s like having a bodyguard standing between your family and financial chaos.

That emergency fund? It’s the launchpad for all your other financial dreams. It’s like once you’ve got it locked down, you’re suddenly clear for takeoff. Invest aggressively. Take those calculated risks. Chase the opportunities without losing sleep over your safety net. At Top Wealth Guide, we’re all about this-emergency preparedness is the first step on the yellow brick road to genuine financial freedom.