Building generational wealth is more than just getting rich yourself. It's about architecting a financial legacy—a system of assets, knowledge, and opportunities designed to grow and transfer from one generation to the next, creating a lasting safety net and a foundation for future success.

In This Guide

- 1 Laying the Groundwork for Lasting Family Wealth

- 2 Building Your Wealth Engine with Smart Investing

- 3 Protecting Your Legacy with Strategic Estate Planning

- 4 Instilling Financial Wisdom in the Next Generation

- 5 Keeping Your Wealth Strategy on Track

- 6 Frequently Asked Questions About Generational Wealth

- 6.1 1. How much money do I need to start creating generational wealth?

- 6.2 2. What's the biggest mistake people make?

- 6.3 3. Is a will enough, or do I really need a trust?

- 6.4 4. How do I balance enjoying life now with saving for the future?

- 6.5 5. Should I pay off my mortgage early or invest?

- 6.6 6. What role does life insurance play?

- 6.7 7. How can I protect our family's assets from a future divorce?

- 6.8 8. What is a "family bank" and how does it work?

- 6.9 9. Is real estate a better investment than stocks?

- 6.10 10. How often should I review and update my plan?

Laying the Groundwork for Lasting Family Wealth

Let's get one thing straight: creating generational wealth doesn't happen by accident. It’s not about a single hot stock tip or getting lucky in a real estate boom. It’s a deliberate, long-term strategy built on a rock-solid foundation. This is where we stop dreaming and start building.

Families that succeed at this have a set of core principles that work in tandem. Think of them as the interlocking gears in a machine built to run for a hundred years, ensuring your family’s security can weather any economic storm and stand the test of time.

The Four Pillars of a Wealth Legacy

A truly durable plan is built on four key areas, each one supporting the others. If you neglect one, the entire structure becomes wobbly.

- Disciplined Financial Habits: This is the bedrock. It means consistent saving, smart budgeting, and making the conscious decision to live below your means to free up capital for investing.

- Smart Investing for the Long Haul: This goes way beyond just buying a few stocks. It means building a diversified portfolio—across different asset classes—that’s engineered for steady, long-term growth that will always outrun inflation.

- Strategic Asset Protection: Making money is only half the battle; keeping it is the other. You have to shield your wealth using smart estate planning tools like trusts and insurance to protect it from excessive taxes, lawsuits, and other unexpected threats.

- Financial Education for Heirs: This might be the most important pillar of all. You have to prepare the next generation to be responsible stewards of the wealth they inherit. Without financial wisdom, wealth disappears fast—a staggering 70% of wealthy families lose it all by the second generation.

The goal is a complete mindset shift: Stop thinking about just earning a paycheck and start building a system that generates wealth for your family indefinitely. This demands a proactive approach to both planning and education.

From Theory to Action

Each of these pillars requires concrete, actionable steps. For instance, you can't have disciplined financial habits without knowing what you're aiming for. Setting clear goals gives you a roadmap that guides every saving and investing decision you make. For a much deeper dive into this, our guide on setting SMART financial goals for a prosperous future provides a clear framework for this critical first step.

Ultimately, laying this groundwork is about instilling a culture of financial responsibility within your family. It's about combining tangible assets with intangible values—like a strong work ethic and financial literacy—to create a legacy that is both wealthy and wise. This is how a simple inheritance is transformed into true generational wealth.

Building Your Wealth Engine with Smart Investing

Once you’ve got a solid financial foundation, it’s time to build the engine that will power your family’s wealth for decades to come. This isn't about chasing hot stock tips or gambling on fleeting trends. It's about methodically constructing a resilient, diversified portfolio designed for one thing: multi-generational growth. The idea is to create a system where your money works for you, compounding over time to turn consistent contributions into a substantial legacy.

A well-crafted investment strategy is the heart of any generational wealth plan. It’s all about balancing different types of assets to manage risk while capturing growth, ensuring your portfolio can ride out economic storms and flourish when times are good.

Diversifying Across Asset Classes

True portfolio resilience isn't found in a single investment. Putting all your eggs in one basket—whether it’s stocks or real estate—exposes your legacy to risks you just don’t need to take. A much smarter approach is to combine different types of investments, where each one plays a unique role in the bigger picture.

- Index Funds and ETFs: For many, these are the bedrock of a long-term portfolio. By investing in broad market indexes like the S&P 500, you’re essentially buying a small piece of hundreds of companies. It's a simple, effective bet on the long-term growth of the economy. This low-cost, set-it-and-forget-it approach is one of the most powerful ways to put compounding to work for you. For a closer look, you might be interested in our deep dive on what index funds are and how they operate.

- Real Estate: Tangible assets like rental properties or Real Estate Investment Trusts (REITs) bring something different to the table. They can generate a steady stream of passive income from rent and tend to appreciate over time, making them a fantastic hedge against inflation.

- Alternative Assets: Modern portfolios often look beyond the usual suspects. This can include private equity, venture capital, and even a strategic, small allocation to digital assets. While these definitely carry more risk, they can also offer outsized growth potential that's hard to find elsewhere.

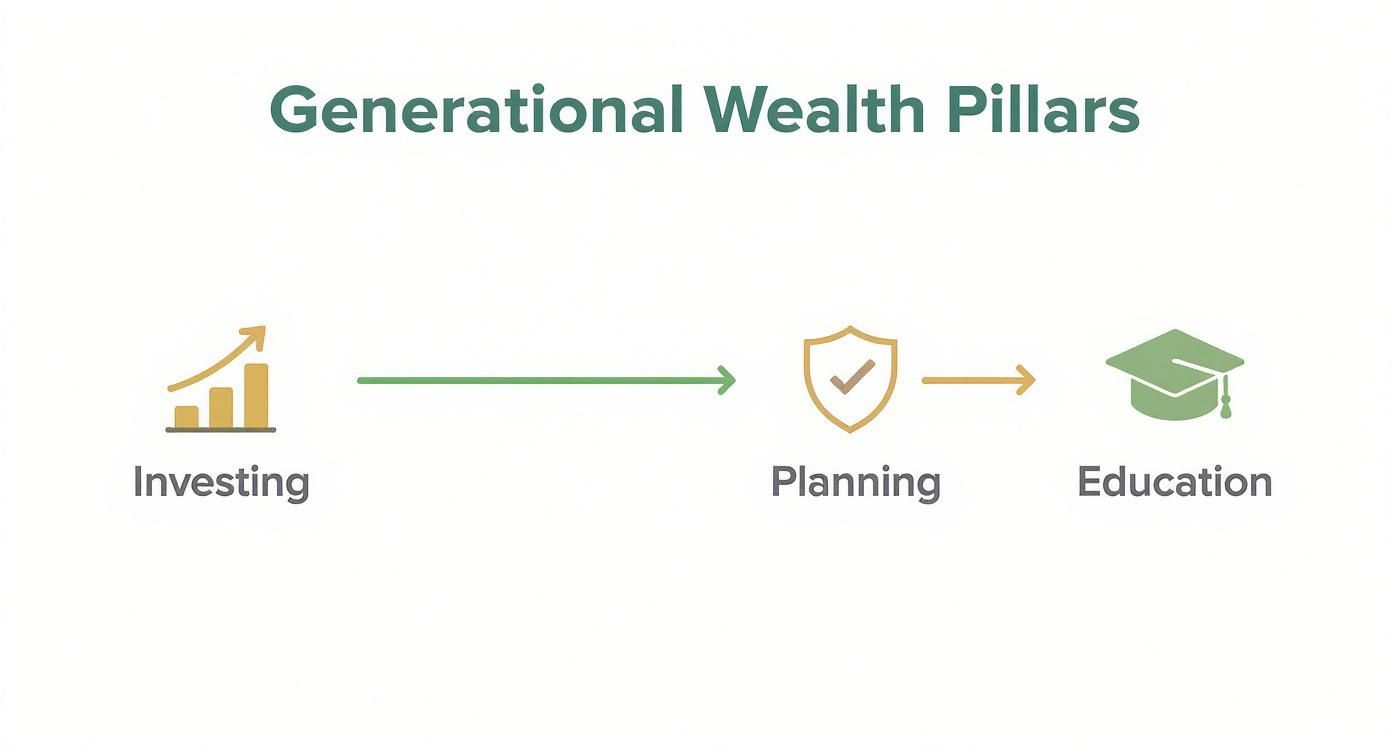

This simple diagram shows how these core pillars—Investing, Planning, and Education—work together to support a lasting financial legacy.

As you can see, investing is the engine, but it needs strategic planning to protect what you build and education to make sure the next generation knows how to keep it going.

The face of wealth is also changing. According to a 2023 Knight Frank report, the global ultra-high-net-worth population grew to 626,619, controlling trillions in assets. Younger investors, especially Millennials and Gen Z, are driving a shift in how this wealth is invested. They're diversifying into venture capital, digital assets, and other passion investments, a trend that could see them reshape wealth management in the coming decades.

Comparing Investment Vehicles for Your Legacy

Choosing the right mix of assets really comes down to your family's specific goals, comfort with risk, and time horizon. This table breaks down the most common investment vehicles to help you see where each might fit into your long-term strategy.

| Investment Vehicle | Long-Term Growth Potential | Typical Risk Level | Liquidity | Management Effort | Primary Role in Portfolio |

|---|---|---|---|---|---|

| Index Funds/ETFs | High | Medium | High | Low | Core growth engine, broad market exposure. |

| Individual Stocks | Very High | High | High | High | Satellite positions for high-conviction ideas. |

| Rental Properties | Medium to High | Medium | Low | High | Income generation, inflation hedge. |

| REITs | Medium | Medium | High | Low | Liquid exposure to real estate income. |

| Bonds | Low | Low | High | Low | Stability, capital preservation. |

| Private Equity | Very High | Very High | Very Low | Low (as a limited partner) | High-growth potential, diversification from public markets. |

A well-balanced portfolio combines several of these, leveraging their unique strengths to build a resilient and powerful wealth-generating engine.

Real-Life Example: The Chen Family's Diversified Engine

The Chen family, first-generation immigrants, began building their wealth engine 30 years ago. They allocated 60% of their investment capital into a low-cost S&P 500 index fund, 30% into rental properties in a growing city, and kept 10% in government bonds for stability. The index fund grew steadily through market ups and downs. The rental properties generated consistent cash flow, which they used to pay down the mortgages and eventually buy another property. During recessions, the bonds acted as their safety net. Today, their diversified engine has not only funded a comfortable retirement but has also created a significant, multi-asset inheritance for their children, whom they are now teaching to manage it.

The Chens' story shows the power of this blended approach. It’s not about finding one "perfect" investment. It’s about building a cohesive system where different assets work together to create a legacy that lasts.

Protecting Your Legacy with Strategic Estate Planning

You’ve put in the work to build a powerful investment engine. It's a massive achievement. But all that effort can be seriously undermined without a clear plan to protect and transfer those assets when the time comes. This is where strategic estate planning stops being an option and becomes a non-negotiable part of your mission.

Too many people see estate planning as something reserved for the ultra-wealthy or an uncomfortable task to put off until old age. That's a dangerous mistake. A well-designed plan is what ensures your assets actually reach your loved ones without being eroded by taxes, legal fees, or family drama. It’s a mental shift from just owning assets to strategically positioning them for a smooth handoff.

The reality is, we're living through the largest wealth transfer in history. Over the next two decades, an estimated $84 trillion will change hands in North America alone, with a significant portion moving from Baby Boomers to their heirs. This historic movement makes having a solid plan more urgent than ever. You can learn more about the global wealth transfer from UBS.

Wills vs. Trusts: Understanding the Core Tools

Your two most fundamental tools are the will and the trust. People often talk about them in the same breath, but they do very different jobs and offer distinct advantages for families trying to build a lasting legacy.

A Last Will and Testament is the baseline—a legal document spelling out who gets what after you're gone. It's an essential starting point, but it comes with a major catch: it has to go through probate. Probate is a court-supervised process that can be slow, expensive, and worst of all, public. The details of your estate become a public record for anyone to see.

A Trust, on the other hand, is a private legal arrangement where you transfer assets to be managed for your beneficiaries. Since the trust technically owns the assets, they sidestep the probate process entirely. This gives you privacy, speed, and a level of control that a simple will just can't offer.

Estate planning isn't just about what happens when you're gone; it's about setting up a structure that protects your family's assets today and ensures they are managed according to your wishes for generations to come.

Comparing Key Estate Planning Structures

Choosing between different types of trusts might seem complicated, but it gets a lot clearer when you focus on their main purpose. A revocable trust gives you flexibility, while an irrevocable trust offers powerful protection.

| Structure | Primary Purpose | Flexibility | Asset Protection | Probate Avoidance |

|---|---|---|---|---|

| Will | Directs asset distribution after death. | High (Can be changed anytime) | Low | No (Goes through probate) |

| Revocable Trust | Manages assets during your life and transfers them after death. | High (You control and can change it) | Low to Medium | Yes |

| Irrevocable Trust | Removes assets from your estate for tax benefits and creditor protection. | Low (Cannot be easily changed) | High | Yes |

For most families just getting started, a revocable living trust is a fantastic tool. You can appoint yourself as the trustee, so you maintain complete control over everything during your lifetime. When you pass away, the successor trustee you named steps in to manage and distribute the assets just as you instructed, completely bypassing the probate courts.

An irrevocable trust is a more advanced move. Once you put assets into it, you give up control. The trade-off? Those assets are generally shielded from creditors, lawsuits, and, most importantly, they're removed from your taxable estate. For larger estates, this can lead to massive savings on estate taxes.

The Strategic Role of Life Insurance

Life insurance is another piece of the puzzle that's often misunderstood when it comes to generational wealth. It does much more than just replace lost income; it serves two vital functions.

-

Providing Immediate Liquidity: Estate taxes, if they apply to you, are typically due in cash within nine months of death. If there isn't enough cash on hand, your heirs could be forced to sell off precious assets—like the family business or real estate—often at a fire-sale price just to pay the tax bill. A life insurance policy delivers an immediate, tax-free payout to cover these costs, preserving the core of your legacy.

-

Acting as a Separate Asset Class: Certain types of permanent life insurance (like Whole or Universal Life) accumulate a cash value that grows on a tax-deferred basis. This cash value becomes another asset you can borrow against or tap into, creating an entirely separate financial vehicle within your overall plan.

A truly effective wealth transfer relies on a thoughtful combination of these tools. For a deeper dive into the specifics, check out our guide on how to transfer wealth to the next generation effectively. In the end, a strategic estate plan is the final, crucial step that ensures the wealth you build actually becomes the legacy you envision.

Instilling Financial Wisdom in the Next Generation

Here’s a hard truth I’ve learned over the years: fortunes rarely outlive the people who build them. The research backs this up, showing that without a solid financial education, even a massive inheritance can vanish in a single generation. The most valuable asset you can pass down isn't the money—it's the wisdom to manage it, preserve it, and make it grow.

This is about more than just opening a savings account for your kids. It’s about intentionally creating a family culture where financial literacy is a core value. The goal is to turn heirs into capable stewards of the family legacy, because generational wealth is ultimately sustained by shared knowledge, not just account balances.

From Allowance to Asset Management

Teaching financial responsibility is a marathon, not a sprint. You have to build concepts on top of each other, starting with simple ideas and moving toward more complex decisions as your kids get older.

- Ages 5-8 (The Basics of Earning and Saving): This is where you introduce the idea that money is earned, not just given. Instead of a blanket allowance, try tying small payments to chores that go beyond basic household duties. A clear jar system with three labels—Save, Spend, and Give—is a fantastic visual tool to teach them how to allocate money from day one.

- Ages 9-12 (Introducing Budgeting and Trade-Offs): At this stage, they're ready for a modest, regular allowance. Sit down with them and create a simple budget for their spending money. This is the perfect time to teach them about trade-offs. If they want that expensive video game, they have to save for it over several weeks. It’s a powerful lesson in patience and delayed gratification.

- Ages 13-17 (First Experiences with Investing and Earning): Encourage them to get a part-time job. This is where you can introduce the magic of compounding. A powerful strategy I’ve seen work wonders is matching their Roth IRA contributions. If they earn $7,000 over a summer, you can contribute that amount to a custodial Roth IRA on their behalf. That one move can turn their high school job into a $1 million+ nest egg by the time they retire.

The point isn't just to teach them how to save money. It's about building the muscle memory for making smart financial choices. You're empowering them with the skills to confidently manage their own finances long before they ever inherit a dime.

Establishing a Family Financial Culture

As your family and your assets grow, those informal money talks need to evolve. You need something more structured. Creating a formal framework ensures that your values are preserved right alongside your capital, shifting the dynamic from entitlement to shared responsibility.

This is more critical now than ever. The next few decades will see an unprecedented shift in global assets. An estimated $84 trillion is expected to be transferred from baby boomers to younger generations by 2045 in North America alone. This massive transfer will reshape everything, with a notable lean toward sustainable and diversity-based investing. Preparing your heirs for this responsibility is paramount.

To build this culture, you need clear communication channels and shared goals that everyone buys into.

Communication vs. Governance Frameworks

Just talking about money isn't enough; you need a system. Here’s a look at how informal family chats can evolve into a robust governance structure that guides your family's wealth for decades.

| Approach | Description | Best For | Real-World Example |

|---|---|---|---|

| Family Meetings | Informal, regular discussions about family finances, goals, and values. Low-stakes and educational. | Younger families and those just starting their wealth journey. | A quarterly "Family Finance Night" where you review savings goals and discuss a basic concept, like what a stock is. |

| Family Mission Statement | A written document outlining the family's core values, goals, and purpose for its wealth. | Families with growing assets who need to align on a shared vision. | The Johnson family writes a mission statement emphasizing education, entrepreneurship, and philanthropy as the pillars of their legacy. |

| Family Council | A formal governing body of family members that makes decisions about shared assets, philanthropy, etc. | Large, multi-generational families with complex assets like a business or foundation. | The Williams family council meets twice a year to vote on philanthropic distributions and review the performance of their investment trust. |

By creating these structures, you build a system of accountability. It ensures decisions are made thoughtfully and collectively, which dramatically reduces the potential for conflict down the line. You're not just passing down assets; you're passing down a process for managing them wisely.

Ultimately, the bedrock of this entire process is financial literacy. Without it, even the most brilliant plans can crumble. To dive deeper into this critical topic, you can learn why financial literacy is the key to building wealth in our detailed article. It truly is the single most important inheritance you can give.

Keeping Your Wealth Strategy on Track

A plan for generational wealth isn't a "set it and forget it" document you shove in a drawer. It’s a living strategy, one that needs to breathe and adapt as life unfolds and the world changes. Think of it as a flight plan for your family’s financial future; you have to constantly check the instruments and make course corrections to navigate turbulence and reach your destination. Active, hands-on management is what separates a good plan from a truly resilient, multi-decade legacy.

The bedrock of this process is measurement. After all, you can't manage what you don't measure. By keeping an eye on a few key numbers, you get a clear, unbiased picture of how you're doing and can spot potential trouble long before it becomes a crisis.

Key Metrics to Monitor

To keep your strategy grounded in reality, you don't need to get lost in a sea of spreadsheets. Just focus on a handful of high-impact metrics that give you a quick, honest snapshot of your financial health.

- Net Worth Growth: This is your ultimate scorecard. Calculate your total net worth (what you own minus what you owe) at the same time every year. A steady, upward trend is the best confirmation that your big-picture strategy is firing on all cylinders.

- Portfolio Performance vs. Benchmarks: It's not enough to just see that your investments went up. How did they perform compared to the market? Pit your portfolio against relevant benchmarks, like the S&P 500 for your US stocks. This tells you if your specific investment choices are actually adding value.

- Cash Flow Analysis: You need to know where the money is going. Track the income generated from your assets—think dividends, rental income, and business distributions—and weigh it against your expenses and tax bills. Positive cash flow is the engine of growth, freeing up capital for reinvestment.

- Progress Toward Specific Goals: Are you funding 529 plans for grandkids? A charitable foundation? Track the balances in these specific accounts against the targets you've set. It's the only way to know if you're truly on pace to meet those future commitments.

The Annual Review Cycle

Tracking these numbers is half the battle; the other half is acting on what they tell you. The most effective way I've seen clients do this is by establishing a formal annual review. This is dedicated time—non-negotiable—to sit down with your core team of advisors: your financial planner, accountant, and estate planning attorney. Together, you can look at the plan from every angle.

This meeting isn't just about numbers, either. It’s about life. Major life events are often the catalyst for the most critical adjustments.

Real-Life Example: The Miller Family's Proactive Plan Adjustment

The Miller family had a comprehensive trust and investment plan all buttoned up. But two years in, their state passed a new inheritance tax law, and on top of that, their eldest daughter got married. During their annual review, their attorney immediately flagged the new law, which would have created a massive, unexpected tax bill down the road. At the same time, their financial advisor pointed out that their daughter's marriage meant her inheritance was now potentially exposed. They quickly amended the trust, creating a special sub-trust for her share to shield it from marital disputes and adjust for the new tax rules. That single review saved them a fortune and a world of heartache.

When to Adjust Your Strategy

While the annual review is your scheduled check-in, some events demand you pick up the phone and call your team immediately. Think of these as mandatory pit stops.

| Trigger Event | Financial Plan Adjustment | Estate Plan Adjustment |

|---|---|---|

| Marriage or Divorce | Update beneficiary designations; adjust budget and goals. | Amend will and trust; consider a prenuptial/postnuptial agreement. |

| Birth of a Child | Open and fund a 529 or custodial account; increase insurance. | Update will/trust to include the new heir and name a guardian. |

| Significant Asset Change | Rebalance portfolio; adjust tax strategy. | Re-evaluate trust funding and potential estate tax liability. |

| Changes in Tax Law | Adjust investment or gifting strategies to remain efficient. | Update trust provisions to align with new regulations. |

Making these periodic tweaks is a normal and necessary part of any sound, long-term plan. A classic example is rebalancing your investments to maintain your target asset allocation as markets shift. To dig deeper into that specific tactic, you can learn more about effective portfolio rebalancing strategies in our comprehensive guide. This kind of active management is what keeps your plan robust, relevant, and ready to safeguard the legacy you’ve worked so hard to build.

Frequently Asked Questions About Generational Wealth

Embarking on the path to create lasting wealth for your family naturally brings up a lot of questions. It's a big goal, and it’s smart to be curious. Here are some of the most common questions I hear, along with straightforward answers to help you get started.

1. How much money do I need to start creating generational wealth?

You don't need a large lump sum. The most important factor is consistency, not the initial amount. You can start by automating small, regular contributions to a low-cost S&P 500 index fund. The core principles—saving consistently, investing for the long term, and living below your means—are the same whether you start with $100 a month or $100,000. The key is to begin now and increase your contributions as your income grows.

2. What's the biggest mistake people make?

The single biggest mistake is focusing exclusively on building financial assets while neglecting to prepare the heirs. Wealth without wisdom is often fleeting. Many families fail to instill financial literacy and a sense of stewardship in the next generation, which is why 70% of wealthy families lose their wealth by the second generation. The education you provide is just as important as the money you leave behind.

3. Is a will enough, or do I really need a trust?

While a will is a crucial starting point, it's often not enough for a true generational wealth plan. A will must go through probate—a public, often slow, and expensive court process. A trust, especially a revocable living trust, bypasses probate, allowing assets to be transferred privately, quickly, and with more control. For protecting assets from creditors and minimizing estate taxes, an irrevocable trust is an even more powerful tool.

4. How do I balance enjoying life now with saving for the future?

This isn't about extreme deprivation; it's about intentionality. A well-crafted financial plan should empower you to live well today while building for tomorrow. The most effective strategy is to "pay yourself first" by automating your savings and investments. Once your contributions to retirement accounts, investment funds, and other long-term goals are automated, the money left over can be enjoyed guilt-free.

5. Should I pay off my mortgage early or invest?

This is a mathematical and psychological question. Financially, if your mortgage interest rate is low (e.g., 3-4%), your money has a high probability of earning a better long-term return in the stock market (historically averaging 7-10% adjusted for inflation). In this case, investing is often the better choice. However, if you have a high-interest mortgage or simply value the peace of mind that comes from being debt-free, paying it off early provides a guaranteed, risk-free return.

6. What role does life insurance play?

Life insurance is a versatile tool. Its primary role is to provide immediate, tax-free liquidity to your heirs. This cash can be used to pay estate taxes, settle debts, and cover other expenses without forcing the sale of assets like a family business or home. Additionally, permanent life insurance policies (like Whole Life) build cash value that grows tax-deferred, effectively creating another asset class within your portfolio.

7. How can I protect our family's assets from a future divorce?

Trusts are a primary line of defense. Assets held in a properly structured irrevocable trust are generally not considered marital property and are therefore shielded in the event of a divorce. For assets held outside of a trust, prenuptial and postnuptial agreements are critical legal documents that can clearly define separate property and protect it for future generations.

8. What is a "family bank" and how does it work?

A family bank is not a literal bank but a formal structure, often an LLC or a trust, that pools family capital. This capital can then be loaned to family members for specific, productive purposes, such as funding education, starting a business, or making a down payment on a home. It operates with formal loan agreements and interest rates, teaching financial discipline while keeping wealth circulating within the family.

9. Is real estate a better investment than stocks?

Neither is inherently "better"; they serve different functions in a diversified portfolio. Stocks (especially through low-cost index funds) offer high liquidity, ease of diversification, and historically strong growth potential. Real estate provides a tangible asset, potential for steady cash flow through rent, significant tax advantages, and acts as a hedge against inflation. A robust generational wealth plan often includes both.

10. How often should I review and update my plan?

Your generational wealth plan should be a living document. A comprehensive review with your team of advisors (financial planner, attorney, accountant) should be conducted at least annually. Furthermore, the plan must be revisited immediately following any major life event, such as a marriage, divorce, birth of a child, significant change in assets, or changes in tax law. Regular maintenance ensures the plan remains aligned with your reality and goals.

At Top Wealth Guide, we're here to give you the knowledge and strategies to build a legacy that lasts. For more proven tactics and exclusive insights to grow and protect your wealth, visit us at https://topwealthguide.com.

This article is for educational purposes only and is not financial or investment advice. Consult a professional before making financial decisions.