Picking the right retirement accounts—it’s like finding a treasure map for tax savings over your lifetime. So, what’s up with the IRS giving us this buffet of account types? Each comes with its own flavor of tax benefits, and they’re tailored to fit different income streams and career chapters.

Here at Top Wealth Guide, we dove into the data pool to scoop up the savviest strategies to max out these benefits. Consider this your cheat sheet: a breakdown of traditional versus Roth options, plus those niche accounts custom-built for the self-employed hustlers out there.

In This Guide

Which Retirement Account Delivers Your Best Tax Win

Traditional 401k and IRA Benefits Hit Your Tax Bill Now

Traditional 401k plans… think of them as the bread and butter of retirement planning. Why? Immediate tax break – that’s why. Drop $10,000 into a traditional 401k, and bam, you just shaved $10,000 off your taxable income. If you’re in the 24% tax bracket, that’s $2,400 saved right off the bat. Sweet, right?

Now, traditional IRAs – similar game, a bit of a twist for high earners. Come 2025, if you’re single pulling in over $87,000 or a married duo earning above $143,000 with workplace plans, your full deduction starts slipping through your fingers. Bummer!

Roth Accounts Pay Off When Tax Rates Rise

Roth 401k and Roth IRA – they play the long game. You pay taxes now, but retire happily ever after without the tax man knocking. Seriously, if you think taxes will climb or your golden years income will bump you up a bracket, Roth’s your bestie.

Imagine a $500,000 Roth IRA cruising at 6.5% annually… in 10 years it balloons to around $939,000 and – drumroll – no taxes on withdrawals. And the cherry on top? Roth IRAs dodge required minimum distributions, so your cash just keeps on growing. The hiccup: in 2025, if you’re a couple making over $240,000 (or single over $161,000), Roth IRA contributions go poof.

Self-Employed Options Maximize Contribution Power

Running your own show? SEP-IRAs and Solo 401k plans are your turbo boost. SEP-IRA lets you drop in up to 25% of your net self-employment dough or $70,000 in 2025 (whichever’s less). But Solo 401k – oh man – takes it up a notch, merging employee and employer contributions for a potential $70,000 yearly stash.

If you’re pulling in $200,000 as a self-made hustler, that $70,000 Solo 401k contribution carves out $16,800 in tax savings at that lovely 24% bracket, while chunking up your retirement fund. These contribution limits really make you ponder… which account sails you smoothly through the choppy waters of future tax scenarios?

Which Account Type Wins the Tax Game

Taxes… the perennial favorite of every dinner party convo. Dive into the trenches of tax strategy, and you’ll find it’s all about one thing: your tax rate now versus later. Are you lower or higher in retirement? Traditional accounts give you that instant hit of gratification-save $5,640 on your 2025 taxes with a $23,500 401k contribution if you’re in the 24% bracket today. Sweet relief. But Roth accounts-they’re like the insurance against future tax hikes. Let a $500,000 Roth IRA grow at 6.5% and boom-$939,000, tax-free, after a decade. Meanwhile, every penny you pull from a traditional IRA gets a tax bite.

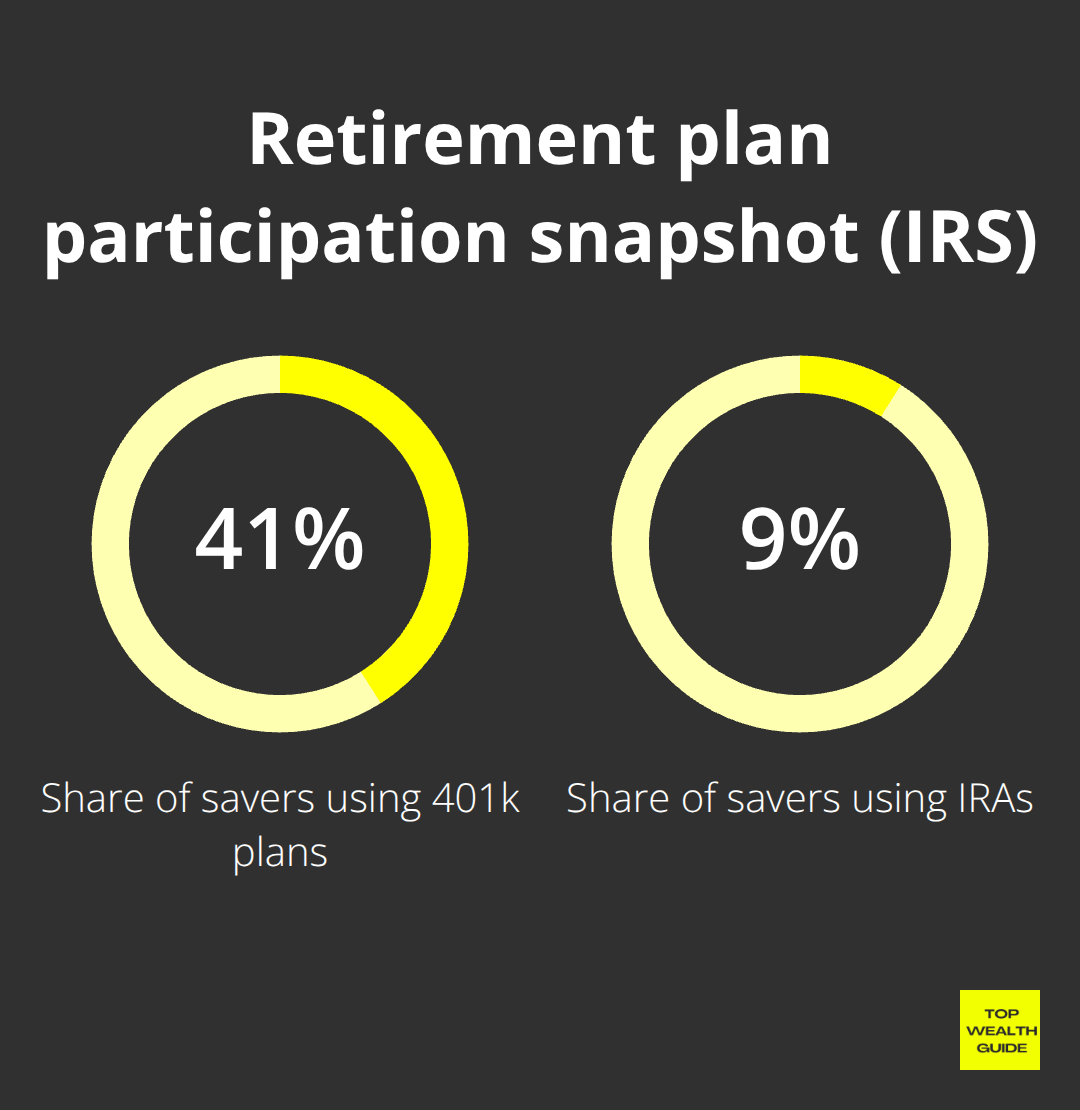

Look at the IRS data… 41.7% are all over those 401k plans, compared to a mere 9.1% embracing IRAs. But wait-income limits, they’re the sneaky game-changers.

Income Caps Block High Earners From Best Options

Enter the income thresholds-those pesky lines in the sand that shake up your retirement strategy. If you’re a top earner, get ready for some frustration. Roth IRA contributions vanish when the family income hits $240,000, or $161,000 for solo high-fliers in 2025. Boom. Traditional IRA deductions? Say goodbye at $87,000 if you’ve got an employer plan.

But 401k? No income limits. That’s why earners between $50,000 and $200,000 tossed in 59% of the retirement dollars in 2018, thank you very much, IRS. And self-employed folks-they laugh in the face of these limits with SEP-IRAs. Toss $70,000 in, no matter the bank balance.

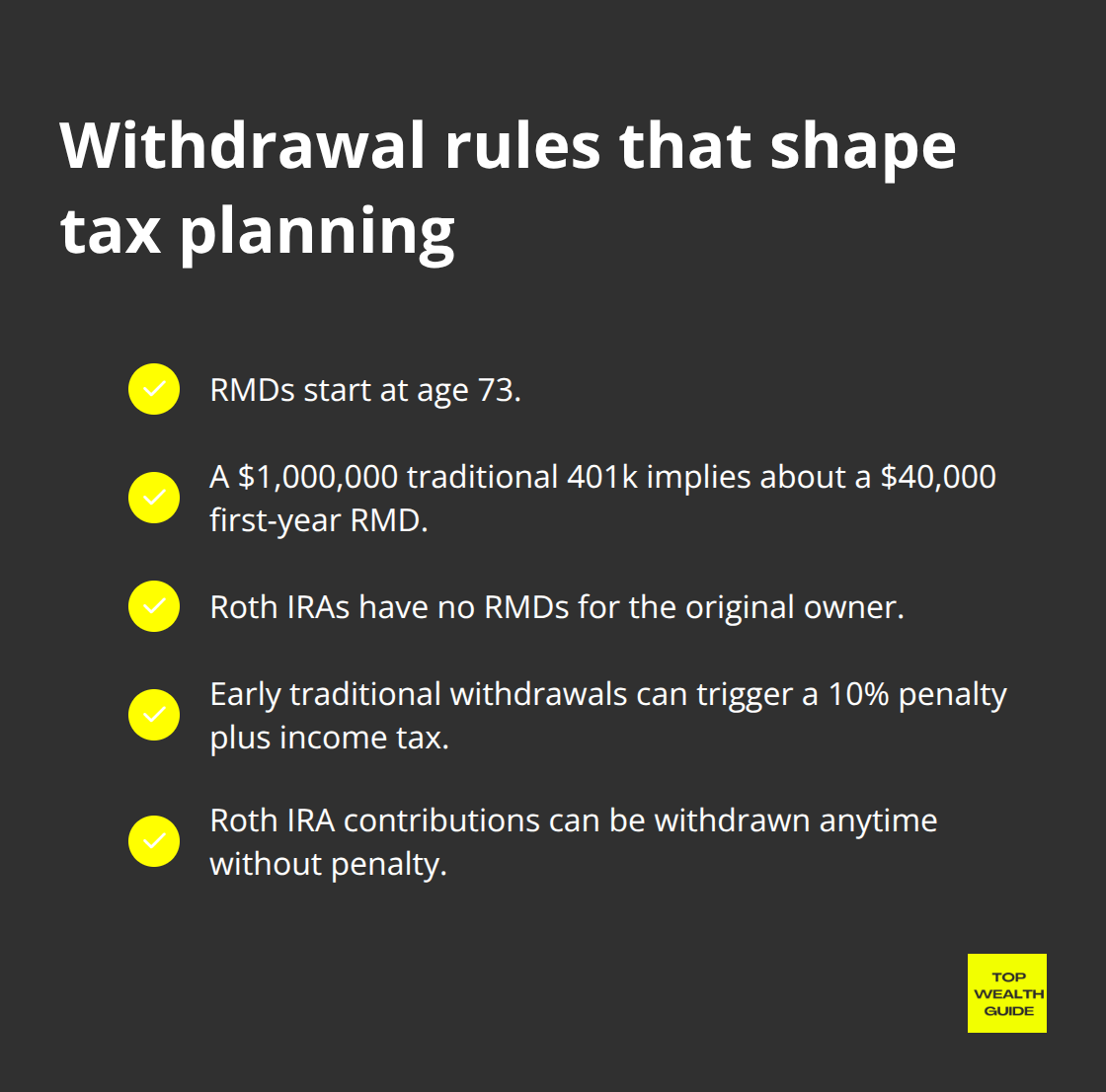

Required Withdrawals Kill Tax Planning Flexibility

Required minimum distributions once you hit 73? They’re the tax planning nightmare. Got a $1 million traditional 401k? Get ready to pull out $40,000 a year whether you’re living lavish or modest. Roth IRAs, though… they let your money keep growing, untouched, no RMDs while you’re around.

It stacks up. Bureau of Labor Statistics tells us 85% of IRA withdrawals in 2018 came from the over-60 crowd, but 15% got hit by early withdrawals, often due to financial curveballs. Here’s where Roth shines: early traditional account withdrawals face a 10% penalty plus regular income tax. Roth? Pull contributions out anytime, penalty-free.

These withdrawal rules? They set the playing field for mixing and matching accounts based on today’s income and tomorrow’s tax bets.

How Do You Build the Perfect Retirement Tax Strategy

Here’s the deal: smart money moves are all about strategy, not crossing your fingers. The wealthy? They don’t just pick a single retirement account and call it a day-they create tax diversification across an array of account types to keep their tax load in check, no matter what decade we’re in. This playbook works ’cause tax rates do a dance, income seesaws, and life is full of surprises that a one-account plan can’t tackle.

Tax Diversification Beats Single Account Strategy

It’s the mix that matters. Combine traditional and Roth accounts based on where taxes are now and where you think they’re heading. Making $80K today but expecting $120K in retirement from pensions and Social Security? Focus on Roth contributions now. Meanwhile, high rollers making $200K should pump up their traditional 401k for a cool $48K tax savings at that 24% bracket-then shift chunks to Roth when the cash flow dips. T. Rowe Price’s take? Savers hitting 15% of income across both account types find flexibility that the one-account crowd just doesn’t have.

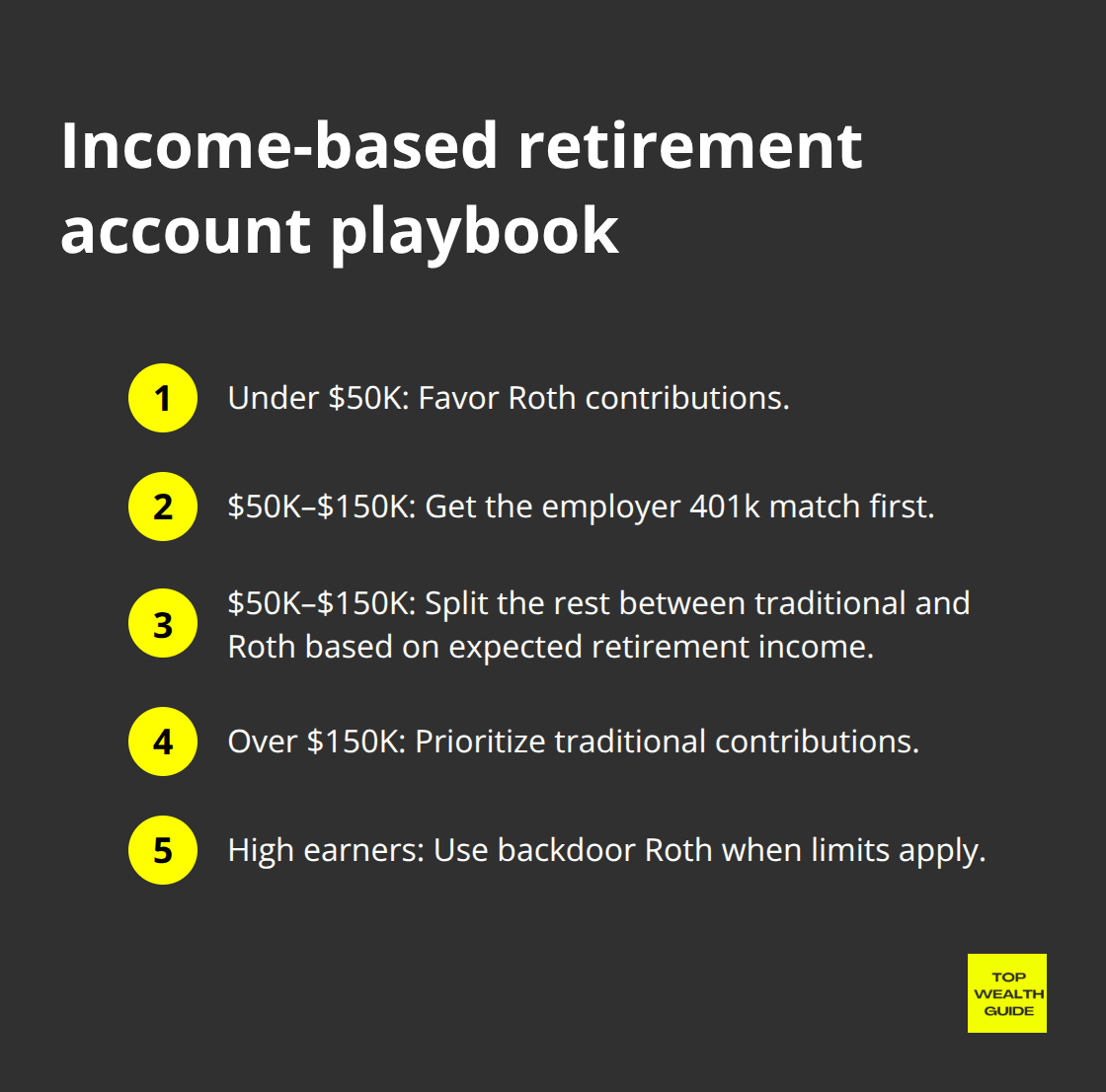

Income-Based Selection Drives Account Choice

Let’s break it down-your income decides where to get the biggest bang from your accounts. Under $50K? Roth is your buddy-your 12% tax bracket now likely beats what’s coming. Earning between $50K and $150K? You’ve got options: snag that employer 401k match first, then divvy up the rest between traditional and Roth depending on what you expect retirement income to look like.

Over $150K? Traditional accounts are your best bet until those pesky income limits butt in (then it’s all about the backdoor Roth conversions).

Conversion Windows Create Tax Arbitrage

Switching traditional IRA funds to Roth during lean income years? Genius. Times like job shifts, early retirement joyrides, or business slowdowns make for primo conversion windows. A $50K move in a year where you’re making just $40K keeps you cruising in the lower tax brackets while giving your money a nice tax-free growth ride. Studies show that Roth conversions can pay off even if future tax rates don’t outpace current ones-turn conventional conversion timing wisdom on its head.

Strategic Withdrawal Sequencing Extends Portfolio Life

The withdrawal sequence matters, big time: dip into taxable accounts first, then traditional accounts, and let those Roth accounts chill ’til last to wring every drop of efficiency from taxes. This sequence lets tax-deferred accounts simmer longer while saving Roth money for the big-ticket years or estate assignments. Financial advisors rave that clients who play this withdrawal order right often stretch retirement funds by another 3-5 years compared to the grab-and-go approach, giving them that extra push towards building lasting wealth.

Final Thoughts

The numbers don’t lie, folks – traditional 401k and IRA accounts are basically tax-saver superheroes that can slash your current bill by thousands – absolutely thousands. Meanwhile, Roth accounts trade off those immediate deductions for decades of sweet, sweet tax-free growth and withdrawals. If you’re self-employed, you’re in for a treat with SEP-IRAs and Solo 401k plans. These bad boys let you stash away a cool $70,000 annually without tripping the income restriction alarms that block the big earners.

So, where do you start? It begins with a deep dive into your income. If you’re pulling in under $50,000, lean into those Roth contributions. For those raking in between $50,000 and $150,000, a mix of traditional and Roth is the way to go. And, for the high flyers making over $150,000, it’s all about maxing out those traditional contributions until income limits nudge you toward alternative retirement accounts.

Tax diversification – that’s the name of the game. Juggling multiple account types gives you flexibility that a single-account strategy just can’t compete with. Time those conversions for low-income years and sequence withdrawals to stretch that portfolio lifespan by a good 3-5 years. Here at Top Wealth Guide, we highly recommend bringing in the big guns – certified financial planners who know retirement tax strategies like the back of their hand – to help you navigate the labyrinthine rules of these wealth-building gems.