The journey of how to become financially independent starts with a single, surprisingly simple question: what’s your number? This isn't just about dreaming of a big pile of money; it's about turning that vague aspiration into a concrete, reachable target. That number, your FI number, is your North Star, and it’s typically calculated as 25 times your expected annual expenses.

Once you know your number, every financial decision you make—from your morning coffee to your career path—gains a new sense of purpose.

In This Guide

- 1 What Does Financial Independence Look Like for You?

- 2 Get a Handle on Your Cash Flow to Skyrocket Your Savings Rate

- 3 Building Your Wealth Engine with Smart Investing

- 4 Accelerate Your Timeline with Passive Income Streams

- 5 Overcoming Roadblocks and Staying the Course

- 6 Frequently Asked Questions About Financial Independence

- 6.1 1. How long does it actually take to become financially independent?

- 6.2 2. What's the single biggest mistake people make on the path to FI?

- 6.3 3. Do I need a huge salary to achieve financial independence?

- 6.4 4. Should I pay off my mortgage or invest extra money?

- 6.5 5. How do I plan for healthcare costs in early retirement?

- 6.6 6. What is the 4% Rule and is it still reliable?

- 6.7 7. Can I use cryptocurrency to get to FI faster?

- 6.8 8. What if my partner isn't on board with the FI journey?

- 6.9 9. Should I focus more on earning more or spending less?

- 6.10 10. How do I handle debt like student loans while pursuing FI?

What Does Financial Independence Look Like for You?

Financial independence isn't a one-size-fits-all destination. Think of it more like a spectrum of freedom. Your first real task is to figure out exactly where on that spectrum you want to land.

This is a deeply personal exercise. It’s about designing a life where your money serves your values, not the other way around. To get started, you need to pin down that tangible number to aim for.

Pinpointing Your FI Number

The most trusted starting point in the FI community is the 4% Rule. It’s a guideline suggesting you can safely withdraw 4% of your investment portfolio each year in retirement without ever running out of money.

To find your magic number, you just flip that rule on its head.

Your FI Number = Your Estimated Annual Expenses x 25

So, if you picture a comfortable life costing you around $60,000 a year, your FI number is $1,500,000 ($60,000 x 25). That's it. This single figure becomes the foundation for your entire strategy—it dictates how much you need to save, how you invest, and how long it will take.

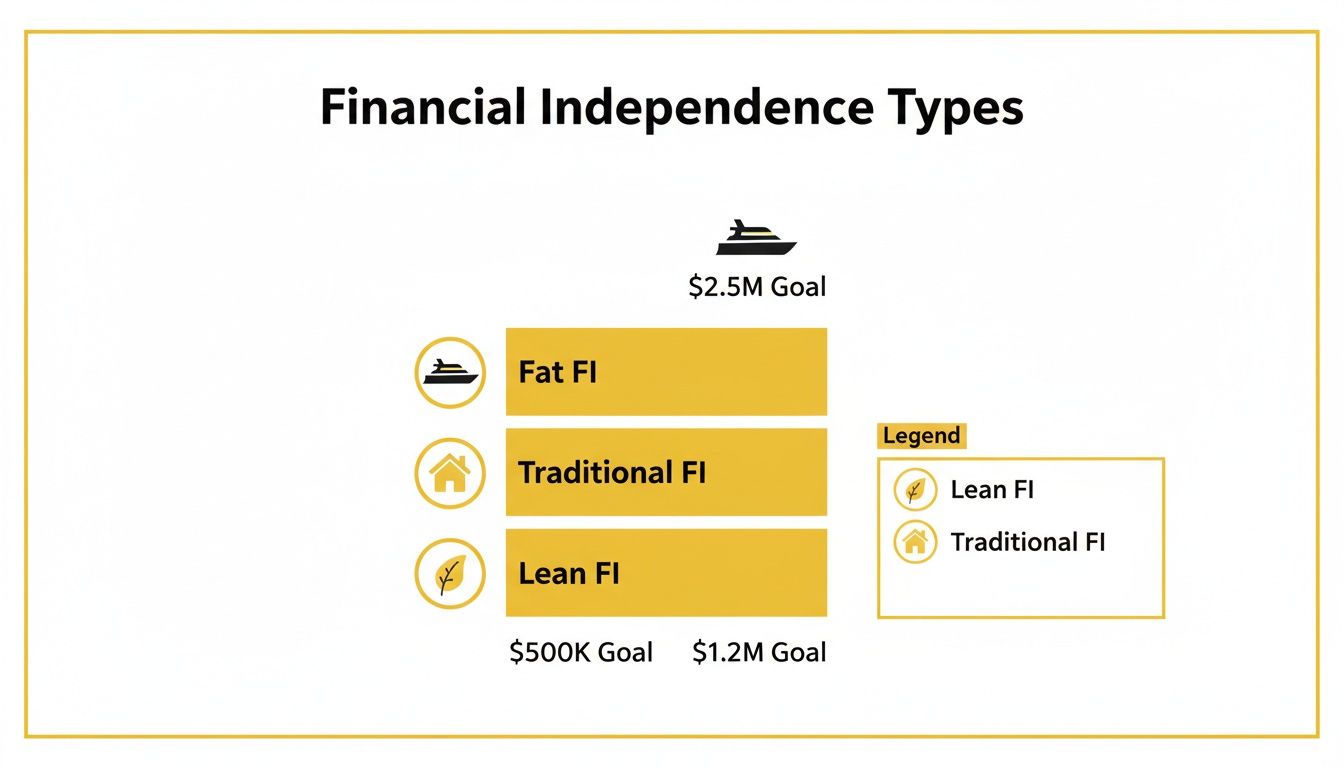

Choose Your FI "Flavor"

Not everyone's vision of a financially free life is the same, and the lifestyle you want has a massive impact on your target number. The FI community generally breaks it down into a few common "flavors."

This is about more than just numbers; it's a chance to get real about what you truly want out of life. For a deeper look into this, check out our guide on how to define wealth beyond money and possessions.

Here’s a quick comparison of the three most common styles:

| FI Type | Description | Target Annual Spending | Estimated FI Number |

|---|---|---|---|

| Lean FI | This is a minimalist path focused on covering the essentials and simple joys. It’s perfect for people who value their time and freedom far more than stuff. | $40,000 | $1,000,000 |

| Traditional FI | Think of a comfortable, standard middle-class lifestyle. It covers all your needs, a good amount of your wants, and allows for regular travel and hobbies. | $80,000 | $2,000,000 |

| Fat FI | This is the luxury tier. It provides for high-end travel, expensive hobbies, and major purchases without ever having to check your bank account. | $120,000+ | $3,000,000+ |

A Tale of Two Paths: A Real-Life Example

Let's look at a real-world example. Imagine two friends, Alex and Ben, who both earn a solid $85,000 a year.

- Alex is aiming for Lean FI. He's an experiences-over-possessions kind of guy. By living in a more affordable city and being mindful of his spending, he keeps his annual expenses at a lean $38,000. His FI number? Just $950,000.

- Ben, on the other hand, wants a Traditional FI lifestyle. He enjoys his larger house in the suburbs, dines out a few times a week, and loves taking big international trips. His lifestyle costs him $65,000 a year, which means his FI number is $1,625,000.

Even with the exact same income, Ben needs to save almost $700,000 more than Alex to reach his goal.

This perfectly illustrates one of the most important truths of this journey: how you spend your money is far more powerful than how much you earn. Getting clear on what "enough" means to you is the critical first step that makes everything else possible.

Get a Handle on Your Cash Flow to Skyrocket Your Savings Rate

If there’s one number that dictates your journey to financial independence, it’s your savings rate. Forget the get-rich-quick schemes; this is about simple math. The bigger the gap between what you earn and what you spend, the faster you get there. Your main job is to widen that gap, and that all comes down to mastering your cash flow.

This isn't about self-deprivation or scrutinizing every coffee purchase. It’s about being intentional. Instead of getting bogged down in tiny details, put your energy where it counts: housing, transportation, and food. I call these the "Big Three," and for a good reason—they eat up over 60% of the typical household budget. Shaving off even a little from these categories makes a huge difference.

Tweak Your Spending Where It Matters Most

Let's put the spreadsheets aside for a second. The real goal is to shift your mindset. You want to start consistently choosing long-term freedom over a short-term dopamine hit.

- Housing: Could you bring in a roommate or rent out a spare room on Airbnb? People call it "house-hacking" for a reason. Maybe downsizing is an option, or even moving to a city with a lower cost of living could slash your biggest expense without hurting your quality of life.

- Transportation: Think about the true cost of your car—gas, insurance, repairs, depreciation. It's a silent wealth killer. Could you swap it for a more efficient model, start using public transit, or even bike to work?

- Food: This doesn’t mean a lifetime of ramen. It’s about planning your meals ahead of time, opting for store brands (they're often identical to the name brands), and cutting back on restaurant meals. That $15 work lunch? Five days a week, it costs you almost $4,000 a year. Think about that.

When you tackle these big-ticket items first, you immediately create more breathing room in your budget. Suddenly, boosting your savings rate doesn't feel like a sacrifice. For a deeper dive, check out our guide on why cash flow management is crucial for wealth building.

The image below gives you a clear picture of how your spending choices directly shape the size of the nest egg you'll need.

As you can see, a "Lean FI" lifestyle requires less than half the investment portfolio of "Traditional FI." That’s the real power of mindful spending right there.

Don't Just Save More, Earn More

Cutting your spending is powerful, but it has a limit. You can only cut so much before you're miserable. Earning more, on the other hand, has no ceiling.

Think of your savings rate as the engine of your FI journey. Cutting expenses is like making that engine more fuel-efficient. Increasing your income is like strapping a turbocharger to it.

Look beyond your 9-to-5. Asking for a raise is a great start, but the real game-changer is building side hustles that can eventually run without you.

Here’s a real-world example:

I once coached a graphic designer named Sarah who started doing freelance logo work on the side. At first, it was just an extra $500 a month. But as she built a name for herself, she created an online course teaching design basics. That course transformed her active side-gig into a semi-passive income stream that now brings in over $2,000 a month. All that extra cash goes straight into her investments, literally shaving years off her FI timeline.

The math is simple and incredibly motivating. The standard FI rule of thumb says you need to invest 25 times your annual expenses. What's incredible is that jumping from a 10% savings rate to a 30% savings rate doesn't just triple your savings—it can cut your time to FI by more than half. You're adding more fuel while your existing investments compound even faster. By pairing smart spending with a drive to earn more, you grab the steering wheel and decide how fast you get to the finish line.

Building Your Wealth Engine with Smart Investing

Getting your cash flow in order and cranking up your savings rate is the essential groundwork for financial independence. But here’s the hard truth: you can’t save your way to freedom. To build real, lasting wealth that can support you for decades, you absolutely must put that money to work.

This is where investing comes in. It's the engine that turns your savings into a self-sustaining machine, working for you around the clock. The entire goal is to outpace inflation and let the magic of compounding transform your nest egg into a sum large enough to fund your life, indefinitely.

Comparing Core Investment Asset Classes

The investment world can feel overwhelming, but for the journey to FI, you really only need to focus on a few key areas. Each one comes with its own blend of risk and potential reward, and the smartest portfolios usually contain a mix.

Most people who successfully reach FI build their wealth on a solid foundation of low-cost, diversified index funds. It's a surprisingly simple but powerful strategy. These funds let you own a tiny sliver of hundreds or even thousands of companies, which is like placing a single bet on the long-term growth of the entire economy. If you're new to the concept, you can learn more about what index funds are and how they work in our detailed guide.

Let's break down how the main investment options compare when your goal is financial independence. This table offers a quick comparison of the big three—stocks, real estate, and crypto—to help you see where each might fit into your strategy.

| Asset Class | Typical Long-Term Return Potential | Risk Level | Liquidity | Best For |

|---|---|---|---|---|

| Stocks (Index Funds) | High (7-10% avg. annually) | Medium to High | High | Building the core of a long-term, hands-off FI portfolio. |

| Real Estate (Physical) | Medium to High | Medium | Low | Generating rental income and building equity with leverage. |

| Cryptocurrencies | Extremely High | Very High | Medium | A small, speculative "satellite" position in a well-diversified portfolio. |

Ultimately, the right mix depends on your personal risk tolerance and timeline. A simple, low-cost index fund portfolio is often the most reliable workhorse for FI, while real estate or a tiny crypto allocation can serve as supplementary engines for those comfortable with the added complexity and risk.

Key Takeaway: For 90% of your journey, a simple, consistent strategy of investing in low-cost stock and bond index funds is the most reliable and time-tested path to financial independence.

Tailoring Your Portfolio to Your Timeline

Your investment mix isn't a "set it and forget it forever" deal. It needs to adapt as you get closer to your FI number. Think about it: a 25-year-old has decades to ride out market storms, while a 40-year-old closing in on their goal needs to be more focused on protecting what they’ve built. This is the art of asset allocation—finding the right balance between stocks and bonds.

Here’s how this plays out in the real world:

- Maria, Age 25: Just starting her career, Maria has a 30+ year runway to FI. She can afford to be aggressive to maximize growth. Her portfolio reflects this: 90% in a total stock market index fund and only 10% in a total bond market index fund.

- David, Age 40: David is well on his way and hopes to punch the clock for the last time in about 10-15 years. He still needs growth, but capital preservation is becoming more important. His portfolio is more balanced at 70% stocks and 30% bonds, giving him a good shot at growth while smoothing out the ride.

The Power of Tax-Advantaged Accounts

Before you put a single dollar into a standard brokerage account, you need to be maxing out your contributions to tax-advantaged accounts. These are your secret weapons: accounts like a 401(k), 403(b), or an Individual Retirement Arrangement (IRA). They are, without a doubt, the ultimate investment accelerators.

Why? Because they offer incredible tax breaks that seriously amplify your returns over the long haul.

- Tax-Deferred Growth: With a Traditional 401(k) or IRA, you get a tax deduction on your contributions today, and the money grows without being taxed year after year. You only pay taxes when you pull it out in retirement.

- Tax-Free Growth: A Roth 401(k) or Roth IRA is even better for many. You contribute with after-tax money, but then your investments grow completely tax-free. Every qualified withdrawal you make in retirement is 100% tax-free.

Treat these accounts like a VIP pass for your money. They shield your investments from the constant drag of taxes, allowing your wealth engine to run faster and more efficiently. This alone can shave years off your journey to FI.

Accelerate Your Timeline with Passive Income Streams

If a high savings rate is the engine of your FI journey, think of passive income as the turbocharger. This is the money you make from the assets you own—not from trading your time for a paycheck. It’s about building systems that work for you, even when you’re sleeping.

Sure, it takes real work upfront to get these streams flowing. But once they’re established, they can pour cash directly into your investments and dramatically shorten your path to freedom. This isn't about some "get rich quick" fantasy; it's a strategic way to make your assets generate the cash you need to buy even more assets. That’s how you create a powerful snowball effect.

Comparing Popular Passive Income Strategies

Not all income streams are created equal. They differ wildly in the time, money, and skill required to get started, not to mention their potential returns. The right choice for you really depends on what you have to work with—your capital, your skills, and how much risk you're comfortable with.

For a deeper dive, our guide on the best passive income ideas is a great place to start.

Here's a quick look at how four of the most common paths stack up:

| Passive Income Stream | Upfront Effort | Initial Capital | Scalability | Real-World Example |

|---|---|---|---|---|

| Dividend Stocks | Low-Medium (Research) | Low to High | High | An investor builds a portfolio of dividend-paying index funds, then automatically reinvests the payouts to buy more shares. |

| Digital Products | High (Creation) | Very Low | Very High | A software developer creates a popular productivity app. After the initial build, each new sale is almost pure profit. |

| Affiliate Marketing | Medium (Content) | Low | Medium | A travel blogger writes detailed guides and earns a commission whenever a reader books a hotel through their affiliate links. |

| Rental Properties | High (Acquisition) | Very High | Medium | Someone buys a duplex, lives in one unit (a strategy called "house hacking"), and rents out the other to cover the mortgage. |

The Global Context of Your FI Journey

It's also worth remembering that where you live has a huge impact on how quickly you can reach financial independence. The stability of your country’s financial system directly affects your opportunities. For instance, in 2025, the Financial Freedom index averaged just 48 points across 175 countries. Yet top-scoring nations like Australia were near 80.

Those numbers reflect massive differences in banking access and capital market development—factors that influence your investment returns, transaction costs, and even the products available to you. You can learn more about these global economic rankings and what they mean for investors.

A Real-Life Passive Income Scenario

Let's make this tangible. Meet Lena, a teacher who makes $60,000 a year. She loves to bake, so she starts a food blog on the side. For the first year, she dedicates 10-15 hours a week to creating recipes and building an audience.

- Year 1: She puts ads on her site and starts earning a modest $100 a month.

- Year 2: She adds affiliate links for baking tools she uses and loves, which brings in another $200 per month.

- Year 3: She creates a beautiful ebook of her 50 best recipes and sells it for $15. Her audience is now big enough that she sells about 40 copies a month, generating another $600.

In just three years, Lena has built a passive income machine that brings in $900 per month, or $10,800 a year. If she invests all of that extra cash into her low-cost index funds, she could potentially shave nearly a decade off her FI timeline.

Lena's story gets to the heart of it: you trade a burst of focused effort today for a stream of income that can flow for years. This is how you finally stop trading time for money and start building a system that funds your freedom.

Overcoming Roadblocks and Staying the Course

The path to financial independence is rarely a straight line. It's a marathon, and you're guaranteed to hit some hurdles that will test your commitment. The goal isn't to magically avoid these problems—it’s to see them coming and have a game plan ready.

One of the biggest and most subtle traps is lifestyle inflation. It’s that natural urge to spend more as you earn more. You get a raise, and suddenly a new car or a bigger apartment seems like a great idea. But this single habit can completely sabotage your savings rate and push your FI date further and further into the future.

Taming Lifestyle Inflation

The best way to fight lifestyle inflation is to get ahead of it. Have a plan for any new money before it even shows up in your bank account.

- Automate Your Raise: If your salary goes up by 3%, bump up your 401(k) or brokerage contributions by that same 3% immediately. Don't even give yourself a chance to get used to the bigger paycheck.

- Try the 50/50 Split: This is a popular and balanced approach. Take half of any new income—a bonus, a raise, a side hustle—and send it straight to your investments. Use the other half to consciously improve your life. This gives you a tangible reward for your hard work without derailing the long-term plan.

- Know Your "Enough": Go back to the vision you created for your ideal life. Does a more expensive car actually get you closer to that vision, or is it just a temporary want? Being clear on your core values makes it easier to resist mindless upgrades.

By giving every new dollar a job, you prevent it from disappearing into lifestyle creep and keep your FI timeline on track.

Nothing rattles an investor's confidence like a market correction. It's tough to watch your portfolio value drop by 20% or more. But how you react in that moment is everything. History has shown time and again that markets eventually recover. Panic-selling, on the other hand, turns a temporary paper loss into a permanent one.

The most successful investors don't try to time the market; they just maximize their time in the market. Your long-term strategy of consistent investing is built to withstand these downturns.

When the market is down, reframe your thinking: you're not losing money, you're buying quality assets at a discount. Continuing your automated investments during a slump is one of the most powerful ways to accelerate your wealth when the recovery begins.

Managing Setbacks and Burnout

Life happens. A sudden job loss, a medical emergency, or an unexpected family crisis can feel like a devastating blow to your plan. This is exactly why a fully-funded emergency fund isn't just a suggestion—it's non-negotiable. It’s your financial shock absorber, letting you handle the crisis without having to sell off your long-term investments at the worst possible time.

Beyond the numbers, your mindset is just as important.

How to Overcome Common Hurdles

| Hurdle | The Trap | The Solution |

|---|---|---|

| Partner Disagreement | Bickering about every single expense. | Shift the focus to the shared life goals FI makes possible, like traveling more or reducing stress. Find a compromise that respects both of your values. |

| Feeling Deprived | Cutting back so aggressively that life feels miserable. | Switch to value-based spending. Be ruthless about cutting costs on things you don't care about so you can spend guilt-free on what you truly love. |

| Slow Progress | Feeling discouraged when your net worth barely budges from one month to the next. | Focus on the metrics you can actually control, like your savings rate and contribution amounts. Celebrate small wins along the way. |

Boosting your financial literacy is another powerful way to build resilience. Research across the globe has shown that even a 1% increase in financial knowledge is linked to a 6.7-point drop in a household's debt-to-income ratio. This knowledge strengthens your financial foundation, making you far less fragile when unexpected challenges arise.

Ultimately, staying the course comes down to having a solid plan, emotional discipline, and a deep connection to your "why." For many, a critical part of that plan involves clearing out existing debt. To learn more, check out our guide on debt elimination tactics for faster financial freedom.

Frequently Asked Questions About Financial Independence

1. How long does it actually take to become financially independent?

Your timeline depends almost entirely on your savings rate, not your income. A higher savings rate allows you to build investments faster while lowering the total amount needed. For example, saving 50% of your income could lead to FI in about 17 years, while saving 20% might take over 35 years.

2. What's the single biggest mistake people make on the path to FI?

The most common mistake is lifestyle inflation—letting your spending increase every time your income does. This prevents your savings rate from growing and pushes your FI date further away. Automating your savings and raises is the best way to combat this.

3. Do I need a huge salary to achieve financial independence?

No. While a high income helps, FI is about the gap between what you earn and what you spend. Someone with a modest salary and a high savings rate can reach FI much faster than a high-earner who spends everything they make.

4. Should I pay off my mortgage or invest extra money?

This is a personal decision. Mathematically, investing often wins if your expected market return is higher than your mortgage interest rate. However, the psychological security of owning your home outright provides a guaranteed, risk-free return and immense peace of mind.

5. How do I plan for healthcare costs in early retirement?

Healthcare is a critical expense that must be included in your FI number. You can explore options on the Affordable Care Act (ACA) marketplace. If you have a high-deductible plan, a Health Savings Account (HSA) is a powerful tool with triple tax advantages.

6. What is the 4% Rule and is it still reliable?

The 4% Rule suggests you can safely withdraw 4% of your portfolio in the first year of retirement and adjust for inflation annually without running out of money. Due to longer lifespans and potentially lower future returns, many experts now recommend a more conservative withdrawal rate of 3% to 3.5% for added safety.

7. Can I use cryptocurrency to get to FI faster?

Cryptocurrency is a highly volatile and speculative asset. While it has high return potential, its risk makes it unsuitable as a core part of an FI strategy. Most financial planners suggest allocating only a very small percentage (1-5%) of your portfolio to it, if any.

8. What if my partner isn't on board with the FI journey?

This is a common challenge. The key is to focus on shared goals and the life FI enables (e.g., more travel, less stress), not just on cutting costs. Frame the conversation around building a better future together and find a compromise that respects both of your values.

9. Should I focus more on earning more or spending less?

Both are crucial, but the order matters. Start by optimizing your spending, as this provides a guaranteed and immediate boost to your savings rate. Once your spending is aligned with your values, shift your focus to increasing your income, which has unlimited potential to accelerate your timeline.

10. How do I handle debt like student loans while pursuing FI?

Prioritize debt based on its interest rate. High-interest debt (>7%), like credit cards, should be eliminated aggressively, as paying it off provides a guaranteed high return. For low-interest debt (<5%), like some mortgages or federal student loans, it can be mathematically better to invest rather than make extra payments, though being completely debt-free has significant psychological benefits.

This article is for educational purposes only and is not financial or investment advice. Consult a professional before making financial decisions.