At its heart, investing in stocks is actually pretty straightforward: you open an investment account, put money in it, and then buy shares of companies or funds. That’s it. By doing this, you're buying a small piece of established businesses, which allows your wealth to grow right alongside them.

This guide provides an in-depth, step-by-step walkthrough for anyone looking to start their investing journey. My goal is to give you the confidence and foundational knowledge to make smart, informed decisions, drawing from years of personal experience and market analysis.

In This Guide

- 1 Your First Steps into Stock Market Investing

- 2 Choosing the Right Brokerage Account for You

- 3 How to Research and Select Your First Stocks

- 4 Placing a Trade and Building Your Portfolio

- 5 Long-Term Habits for Successful Investing

- 6 Frequently Asked Questions (FAQ)

- 6.1 1. How much money do I actually need to start investing in stocks?

- 6.2 2. What's the real difference between a stock and an ETF?

- 6.3 3. How often should I check my portfolio?

- 6.4 4. Is it better to pick my own stocks or just use a robo-advisor?

- 6.5 5. What are dividends?

- 6.6 6. What are the biggest risks of investing in stocks?

- 6.7 7. How do taxes work on my stock market profits?

- 6.8 8. What is dollar-cost averaging (DCA)?

- 6.9 9. Can I lose more money than I invested?

- 6.10 10. Where can I find reliable information for stock research?

Your First Steps into Stock Market Investing

Jumping into the stock market can feel like a huge leap, but it remains one of the most powerful ways to build real, long-term wealth. A stock is just a slice of ownership in a public company. When you buy a share of, say, Microsoft or Amazon, you become a part-owner. You get a claim on a tiny fraction of its assets and profits. This is the whole idea behind it—you’re investing in the future success of these businesses.

The opportunity here is massive and has grown exponentially. Back in 1980, the total value of all stocks globally was around $2.5 trillion. Fast forward to the end of 2023, and that number had ballooned to an incredible $111 trillion. That’s a 44-fold increase, showing just how much the investing world has expanded.

Choosing Your Investing Path

Before you even think about buying, you need to decide on your basic approach. You really have two main choices: picking individual companies or buying into funds.

| Investing Style | Description | Pros | Cons |

|---|---|---|---|

| Individual Stocks | You research and purchase shares of specific companies you believe will perform well. | Higher potential returns; direct ownership in companies. | Higher risk; requires significant research and time. |

| Funds (ETFs/Mutuals) | You buy a single investment that holds a diverse collection of many different stocks. | Instant diversification; lower risk; less hands-on. | Returns are an average of the market; management fees. |

For most beginners, starting with funds like a broad-market ETF is a fantastic way to get instant diversification and reduce risk. For anyone just starting out, our guide on how to start investing for beginners is the perfect place to build a solid foundation.

Selecting the Right Account Type

Just as crucial as what you buy is where you hold it. Your investment account is the home for all your stocks and funds, and the type you choose matters a lot.

The account you choose can have a significant impact on your tax obligations and long-term returns. Understanding the difference between a standard brokerage account and a retirement account is a critical first step.

A standard brokerage account is the most flexible option. There are no limits on how much you can contribute, but you will owe capital gains taxes on your profits when you sell.

On the other hand, a tax-advantaged retirement account like a Roth IRA comes with incredible tax perks. With a Roth IRA, your investments can grow completely tax-free, and you pay zero tax on your withdrawals once you retire. Making this one choice early on can literally save you thousands of dollars over your investing lifetime.

Choosing the Right Brokerage Account for You

Think of your brokerage account as your home base for investing. It's the platform you'll use to actually buy and sell stocks, so picking the right one is a huge first step. The account you choose will shape everything—from the fees you pay to the research tools you can access.

The options out there are all over the map. You've got everything from old-school, advice-heavy firms to slick apps you can run from your phone. There's no single "best" choice; it all comes down to what you need, what you're willing to spend, and how hands-on you want to be. For a more detailed look, it’s worth understanding what an investment account is and how they work behind the scenes.

This chart lays out the two main roads you can take, helping you figure out if a DIY approach or an automated one makes more sense for you.

Ultimately, you have to know where you're going before you can pick the right vehicle to get you there. Your end goal will point you toward either a DIY or an automated strategy.

Comparing Brokerage Account Types

To make a smart decision, you first need to get a handle on the main types of brokers. Each one caters to a different kind of investor, whether you’re a total beginner looking for guidance or a confident DIY-er who wants to keep costs rock-bottom.

Real-Life Example: My retired uncle sticks with a full-service broker because he really values having a personal advisor he can call for his retirement portfolio. On the other hand, my tech-savvy cousin, who is just focused on long-term growth, went with a robo-advisor. She loves the low fees and the "set-it-and-forget-it" convenience.

The right platform isn’t the one with the most bells and whistles; it’s the one that actually fits your financial goals, the time you're willing to commit, and your overall comfort level. Always check the fees, investment options, and support before you sign up.

To help you visualize the differences, here’s a quick comparison of the three main players in the brokerage world.

| Feature | Full-Service Broker | Discount Broker | Robo-Advisor |

|---|---|---|---|

| Best For | High-net-worth individuals or those who want comprehensive financial planning. | DIY investors who are comfortable making their own decisions and want to minimize costs. | Beginners or hands-off investors who prefer an automated, algorithm-driven approach. |

| Fees | Higher, often a percentage of assets managed (1-2%), plus potential commissions. | Low to zero commissions on stock/ETF trades. May have other minor service fees. | Lower management fees, usually a small percentage of your balance (around 0.25-0.50%). |

| Minimum Deposit | Often high, sometimes requiring $25,000 or more to get a dedicated advisor. | Generally low to none. Many platforms have a $0 account minimum, making them very accessible. | Very low. Most let you start with as little as $1, and many have no minimum at all. |

| Investor Control | Collaborative. You work with an advisor but still have the final say. | High. You are in the driver's seat for all buying and selling decisions. | Low. The algorithm automatically selects and manages your investments for you. |

| Support & Tools | Extensive. Dedicated advisors, estate planning, tax guidance, and in-house research. | Robust. Offers a wide range of research tools, charting software, and educational content. | Limited. Support is mainly digital (chat/email), focusing on goal-setting tools. |

As you can see, it’s all about trade-offs. If you want white-glove service and don't mind paying for it, a full-service broker is a solid choice. For most new investors, though, a discount broker or a robo-advisor usually hits that sweet spot of low costs and powerful, user-friendly tools to start building wealth.

How to Research and Select Your First Stocks

Alright, your brokerage account is funded and ready to go. Now for the exciting part—actually finding great companies to invest in. This isn't about chasing hot tips or getting swept up in market hype. It's about doing a bit of homework to make smart, informed decisions.

The heart of this process is something called fundamental analysis. It sounds technical, but all it really means is checking out a company's financial health and future prospects before you put your money on the line.

Ultimately, you're just trying to answer a few straightforward questions: Is this company making money? Is it growing? And is its stock selling for a fair price?

Unpacking the Key Numbers

When you start digging into a company, you’ll run into a wall of acronyms and ratios. Don't get intimidated. You don't need a finance degree to make sense of them. Just a few key metrics can tell you most of what you need to know.

Think of it like checking the vital signs of a business. Here are the most important ones to get you started:

- Earnings Per Share (EPS): This is a clean, simple metric that shows how much profit the company is generating for each outstanding share of its stock. You want to see this number growing consistently over time. It's a fantastic sign of a healthy, expanding business.

- Price-to-Earnings (P/E) Ratio: This ratio compares the company's share price to its earnings. It's a quick way to gauge whether a stock is expensive or cheap relative to its peers or its own history. A high P/E isn't necessarily bad; it often means investors are optimistic and expect big growth ahead.

- Return on Equity (ROE): This one measures how well the company's management is using the money you've invested to generate profits. As a rule of thumb, an ROE consistently above 15% often points to a well-run business with a strong financial position.

A Real-World Example: Microsoft Corp (MSFT)

Let's put this into practice. Say you're thinking about investing in Microsoft. Instead of buying it just because you use Windows or Office, you'd do a quick financial health check.

First, you'd head over to their investor relations website and pull up their latest annual report (also known as a 10-K). You’d quickly see that Microsoft's EPS has been on a steady upward climb for years, fueled by the massive growth in its cloud computing (Azure) and subscription services. That’s a big green flag.

Next, you'd look at its P/E ratio. Is it 25? 35? You'd then compare that number to other tech giants like Apple or Google. If Microsoft's P/E is way higher, you'd dig a little deeper to figure out why. Is the market expecting something huge from them? This simple comparison gives you crucial context that a number alone can't provide.

Looking Beyond the Financials

Numbers tell you what has happened, but they don't tell the whole story. To really understand an investment, you have to look at the business itself. This is what we call qualitative analysis.

A great company can be a terrible investment if you pay too high a price for it. Likewise, a statistically cheap company with a declining business is a value trap. The sweet spot is finding a quality business at a fair price.

Before you invest in any company, ask yourself these three simple questions:

- Do I actually understand how this company makes money? Could you explain it to a friend in under a minute? If the business model is too complicated to grasp, it’s probably best to steer clear for now.

- What's its competitive advantage? What stops another company from coming in and stealing all its customers? This could be a powerful brand like Apple, a network effect like Meta, or the high costs of switching like with Microsoft's enterprise software.

- Do I trust the management team? Take a few minutes to read the CEO’s latest annual letter to shareholders. Do they sound honest, transparent, and focused on creating long-term value? Or are they just spouting corporate jargon?

Combining this qualitative check with your financial review gives you a solid, repeatable process for picking stocks. For a much deeper dive, check out our guide on investment research methods the pros don't want you to know. This disciplined approach will help you make choices based on solid research, not just random market noise.

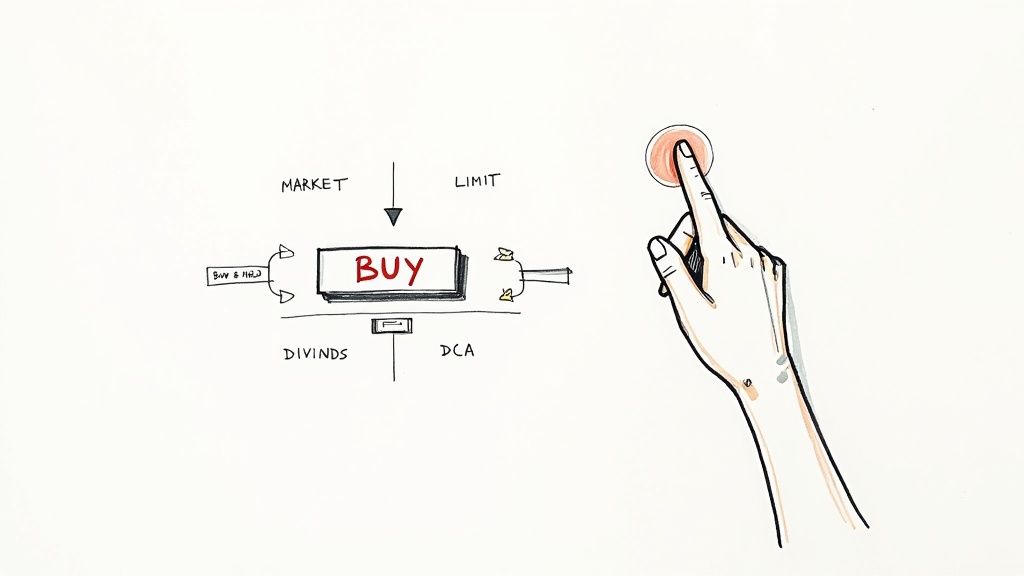

Placing a Trade and Building Your Portfolio

You’ve crunched the numbers, read the reports, and finally picked a company you believe in. Great! Now comes the exciting part: turning your research into a real investment. Actually buying the stock is a crucial step, and knowing how to buy can make a real difference in the price you pay.

When you open your brokerage app to place a trade, you'll see a few options. The two most important ones for new investors are the market order and the limit order. Getting this right is your first big move toward smart, disciplined investing.

Executing Your First Stock Purchase

Let's say you've decided to buy 10 shares of Company XYZ. If you use a market order, you're telling your broker, "Get me these shares right now at whatever the best price is." It’s fast and practically guarantees your order will get filled. The downside? You have zero control over the price. On a choppy day, the stock price could tick up in the seconds between you clicking "buy" and the trade actually executing, meaning you could end up paying more than you expected.

This is where a limit order gives you control. With a limit order, you tell your broker the maximum price you're willing to pay. For example, you can set a limit order to buy XYZ at $50 per share. Your order will only go through if the broker can get it for $50 or less. This protects you from overpaying, but there's a catch: if the stock never dips to your price, your order might not get filled at all.

Understanding Common Order Types

The table below summarizes the key order types, what they do, and when they are most useful for an investor.

| Order Type | What It Does | Best Used When… | Real-World Example |

|---|---|---|---|

| Market Order | Buys or sells a stock immediately at the current best available price. | …you prioritize speed over price. Best for large, highly-liquid stocks like Apple (AAPL) where the price is stable. | You want to buy 10 shares of a big company right now and are okay if the price moves a few cents. |

| Limit Order | Buys or sells a stock only at a specific price or better. | …you want to control the exact price you pay. Crucial for less-traded stocks or during volatile market periods. | You want to buy XYZ stock, but only if its price drops to $50.00 per share. You set a limit order and wait. |

| Stop Order | Becomes a market order to buy or sell once a stock reaches a certain "stop price." | …you want to protect profits or limit losses. A "stop-loss" order automatically sells if a stock falls to your price. | You own a stock at $60 and set a stop-loss at $55. If it falls to $55, your order triggers to sell and limit your loss. |

For most beginners, getting into the habit of using limit orders is a great discipline. It prevents nasty surprises and puts you in control.

Assembling a Diversified Portfolio

Owning shares in just one or two companies is like betting your entire savings on a single hand of poker. It's incredibly risky. If one of those companies hits a rough patch, your entire investment could suffer. That’s why we have diversification—the classic rule of not putting all your eggs in one basket. By spreading your money across different companies, industries, and even asset classes, you cushion yourself from the inevitable ups and downs of any single investment.

A well-diversified portfolio is your primary defense against market volatility. It ensures that poor performance from one investment doesn't sink your entire ship, allowing the winners to carry you forward over the long term.

Here are a few time-tested strategies for building out your holdings:

- Buy-and-Hold: This is the cornerstone of long-term wealth building. You buy shares of high-quality companies or broad-market ETFs and plan to hold them for years, tuning out the day-to-day market noise.

- Dividend Investing: This strategy focuses on buying stocks from established companies that share their profits with shareholders through dividends. You can pocket the cash or, even better, reinvest it to buy more shares and let compounding work its magic.

- Dollar-Cost Averaging (DCA): This is all about consistency. You invest a fixed amount of money at regular intervals—say, $200 every month. This approach forces you to buy more shares when prices are low and fewer when they're high, smoothing out your average cost over time.

Many successful investors use a mix of these strategies. The good news is that many of the best investment apps for beginners make it easy to set up automated investing plans.

Long-Term Habits for Successful Investing

https://www.youtube.com/embed/F1cghFu9zBs

If you want to find real success in the stock market, you need to know it's not about making lucky guesses or trying to perfectly time every market dip and spike. It's really about discipline, patience, and building a set of habits that keep your emotions on the sidelines while you focus on the long-term goal. This is the mindset that separates someone who simply buys stocks from a true investor.

Time is easily the most powerful tool you have. Sure, the market's day-to-day moves are completely unpredictable, but its long-term trend has consistently pointed up. Take the S&P 500, for example. It has posted an average annual compounded return of around 13.6% over the last decade. That kind of historical performance, as you can see in this breakdown of S&P 500 returns on Nasdaq.com, is exactly why a patient, long-view strategy works so well.

Don't Obsess Over Daily Moves

One of the worst things you can do as a new investor is get hooked on checking your portfolio every single day. Those daily swings are just market noise. When you react to them, you’re far more likely to sell in a panic when things are down—which is the exact opposite of what you should be doing.

A much better, saner approach is to schedule your check-ins. A quarterly or even semi-annual review is usually more than enough. It gives you a chance to see if you need to rebalance anything without getting caught up in the emotional rollercoaster of short-term headlines.

Knowing When to Let a Stock Go

Selling is just as critical as buying, and your reasons for doing so need to be grounded in logic, not fear. A stock's price falling isn't, on its own, a good enough reason to hit the sell button.

You need a clear game plan for selling. I generally only consider selling a stock when one of these conditions is met:

- The fundamentals have changed. The original reason I invested is gone. Maybe the company lost its competitive edge, the leadership took a wrong turn, or its financial health is deteriorating.

- A much better opportunity has appeared. My capital could be put to better use in another investment that offers more potential.

- My portfolio is out of whack. If a single stock has grown so much that it's now a dangerously large chunk of my portfolio, it's smart to trim the position and lock in some gains to manage risk.

Dodging the Classic Beginner Traps

So many new investors stumble into the same predictable traps. Just knowing what they are is half the battle.

The biggest threat to your long-term returns is often your own behavior. Chasing hype, abandoning your strategy during a downturn, or ignoring the silent drag of fees can undo years of patient saving and investing.

Here are a few of the most common mistakes I've seen derail people over the years:

- Chasing "Hot Tips": Hearing about a "sure thing" on social media or from a friend is a huge red flag. These "hot stocks" are often incredibly volatile and rarely have the solid business fundamentals you need for real, long-term growth.

- Emotional Investing: Never, ever make decisions out of fear or greed. You created a strategy for a reason—stick to it, whether the market is soaring or sinking.

- Ignoring Fees and Taxes: Those small fees might not seem like much, but they can eat away at your returns over decades. You also need to understand how taxes work, especially the difference between short-term and long-term capital gains, to make sure you keep more of your profits.

By cultivating these habits, you build a portfolio that can weather the inevitable storms. A great way to enforce this discipline automatically is to master dollar-cost averaging for steady wealth growth, which smooths out volatility and takes emotion out of the equation.

Frequently Asked Questions (FAQ)

1. How much money do I actually need to start investing in stocks?

You can start with very little money. Most online brokers have no account minimums, and with fractional shares, you can buy a piece of a company for as little as $1. The key is to start with an amount you're comfortable with and build the habit of investing regularly.

2. What's the real difference between a stock and an ETF?

A stock represents ownership in a single company (e.g., Apple). An ETF (Exchange-Traded Fund) is a basket of many different stocks (e.g., an S&P 500 ETF holds shares in 500 companies). For beginners, ETFs provide instant diversification, which is a great way to manage risk.

3. How often should I check my portfolio?

For long-term investors, checking your portfolio once a quarter is plenty. Checking too frequently can lead to emotional decisions based on short-term market noise rather than long-term fundamentals.

4. Is it better to pick my own stocks or just use a robo-advisor?

This depends on your goals and interest. If you enjoy research and want control, picking stocks can be rewarding. If you prefer a hands-off, automated approach, a robo-advisor is an excellent choice that provides professional management for a low fee.

5. What are dividends?

Dividends are a portion of a company's profits paid out to its shareholders, usually quarterly. They are a way for companies to share their success with investors. You can take them as cash or reinvest them to buy more shares, which accelerates wealth through compounding.

6. What are the biggest risks of investing in stocks?

The primary risk is market risk—the value of your stocks can go down. A company can perform poorly, or an economic downturn can affect the entire market. Diversification is the most effective tool to mitigate this risk, as it spreads your investment across many assets so one poor performer doesn't sink your portfolio.

7. How do taxes work on my stock market profits?

In a standard brokerage account, you pay capital gains tax on profits when you sell. If you hold the stock for more than a year, you pay a lower long-term capital gains rate. If you hold it for a year or less, you pay the higher short-term rate, which is the same as your regular income tax rate.

8. What is dollar-cost averaging (DCA)?

DCA is the strategy of investing a fixed amount of money at regular intervals, regardless of market conditions. For example, investing $100 every month. This approach helps reduce risk by averaging out your purchase price over time.

9. Can I lose more money than I invested?

For a typical investor buying stocks or ETFs, the answer is no. The maximum you can lose is the amount you invested. A stock's value can drop to zero, but not below. Only advanced strategies like short-selling carry the risk of losing more than your initial investment.

10. Where can I find reliable information for stock research?

Start with the company's official "Investor Relations" website for annual reports (10-K). Reputable financial news sources like The Wall Street Journal and Bloomberg are also excellent. Finally, most brokerage platforms offer a wealth of free research tools and analyst reports for their clients.

At Top Wealth Guide, our mission is to provide you with the knowledge and tools needed to build lasting wealth. From mastering stock market fundamentals to exploring advanced investment strategies, we're here to guide you every step of the way. Discover more insights and secure your financial future by visiting us at https://topwealthguide.com.

This article is for educational purposes only and is not financial or investment advice. Consult a professional before making financial decisions.